By Andrew Stowers

Updated May 2, 2026

Fixed income ETFs are the most misused category in retail investing.

Investors who understand them use these funds to generate steady income, reduce portfolio volatility, and strategically position for interest rate cycles. Investors who don’t understand them buy the wrong duration at the wrong time — and wonder why their ‘safe’ bond fund fell 20% while stocks were still rising.

The combination of our ETF Investing Guide and this guide here cover everything you need to use fixed income ETFs correctly: what they are, how they work, the full range of types available, the interest rate mechanics that determine their actual behaviour, the best funds by category, and how to fit them into a complete portfolio.

What Are Fixed Income ETFs? (Definition and How They Work)

| Quick Answer

Fixed income ETFs are exchange-traded funds that hold portfolios of bonds or other debt instruments. They trade on exchanges like stocks, provide regular income distributions from the interest payments collected on their holdings, and offer instant fixed income diversification without the minimum investment required to build an individual bond portfolio. |

Fixed income ETFs package a portfolio of bonds into a single, exchange-traded security. Rather than purchasing an individual Treasury bond with a $1,000 minimum or a corporate bond requiring a larger ticket, an investor can gain exposure to hundreds or thousands of bonds for the price of a single ETF share.

How Income Distributions Work

The bonds inside a fixed income ETF pay coupon interest on their face values. The ETF collects these payments and distributes them to shareholders — typically monthly. This regular income stream is one of the primary reasons investors hold bond ETFs, particularly in retirement accounts or income-focused portfolios.

Unlike individual bonds, which pay a fixed coupon on a known schedule until maturity, ETF distributions vary slightly over time as the portfolio is rebalanced. When older bonds mature or are sold and replaced by new bonds at different yields, the ETF’s income profile shifts gradually with market conditions.

The Critical Structural Difference: No Maturity Date

Bond ETFs do not mature. An individual bond held to maturity guarantees return of face value regardless of what happens to interest rates in the interim. A bond ETF has no maturity date — it continuously rolls its positions, maintaining a target duration profile. If you buy a bond ETF when interest rates are low and rates subsequently rise significantly, the fund’s share price falls. Unlike an individual bond, there is no future date at which you are guaranteed to receive your principal back at a specific value.

This is the most important structural fact about fixed income ETFs. Understanding it prevents the most common bond ETF mistake: treating them as cash equivalents rather than as rate-sensitive instruments.

The Six Types of Fixed Income ETFs Every Investor Should Know

| The Six Categories

Government bond ETFs: Bonds issued by national governments, often used for stability and lower credit risk. Corporate bond ETFs: Bonds issued by companies, typically offering higher yields than government bonds with added credit risk. Municipal bond ETFs: Bonds issued by state and local governments, often used for tax-advantaged income. High-yield ETFs: Lower-rated corporate bonds that offer higher income potential with higher default risk. TIPS ETFs: Treasury Inflation-Protected Securities designed to help protect purchasing power during inflationary periods. International bond ETFs: Bonds issued outside the U.S., adding geographic diversification and potential currency exposure. |

1. Government Bond ETFs

Government bond ETFs hold U.S. Treasury securities (bills, notes, and bonds) or other sovereign debt. They carry the highest credit quality available — backed by the full faith and credit of the U.S. government — and the lowest yield of any fixed income category. They are the primary vehicle for capital preservation and flight-to-quality positioning during equity market stress. Sub-categories exist by duration: short-term (1-3 year), intermediate (3-10 year), and long-term (10-30 year) Treasury ETFs.

2. Corporate Bond ETFs

Corporate bond ETFs hold debt issued by companies — rated investment-grade (BBB/Baa and above). They offer higher yields than Treasuries in exchange for credit risk: the possibility that the issuing company defaults. Investment-grade corporate bond ETFs are a middle-ground option between the safety of Treasuries and the higher yield (and higher risk) of high-yield funds.

3. Municipal Bond ETFs

Municipal bond ETFs hold debt issued by U.S. state and local governments. Their defining feature is federal tax exemption on interest income — making them particularly valuable for investors in higher tax brackets. A municipal bond ETF yielding 3% pre-tax is equivalent to approximately 4.2% for an investor in the 28% federal bracket. Always compare municipal yields on an after-tax basis when evaluating them against taxable alternatives.

4. High-Yield ETFs

High-yield ETFs hold below-investment-grade corporate bonds — rated BB/Ba and below, commonly called ‘junk bonds.’ They offer the highest yields of any investment-grade fixed income category, reflecting higher credit risk and default rates. An important behavioral note: high-yield ETFs correlate strongly with equities during market stress — when credit markets seize up, high-yield ETFs can fall as sharply as equity ETFs. They do not provide the diversification benefit that government or investment-grade bonds typically offer.

5. TIPS ETFs

TIPS — Treasury Inflation-Protected Securities — are U.S. government bonds whose principal adjusts with the Consumer Price Index. TIPS ETFs provide a real yield (return above inflation) rather than a nominal yield. When inflation rises, the principal increases and so does the interest payment. They are the primary tool for protecting fixed income returns against inflation erosion, particularly relevant when CPI is elevated or uncertain.

6. International Bond ETFs

International bond ETFs hold sovereign or corporate debt from outside the U.S. They add geographic diversification to a fixed income portfolio. Currency risk is an important consideration — an unhedged international bond ETF’s returns are affected by USD/foreign currency movements. Currency-hedged versions are available for investors who want purely local-currency bond exposure without FX overlay.

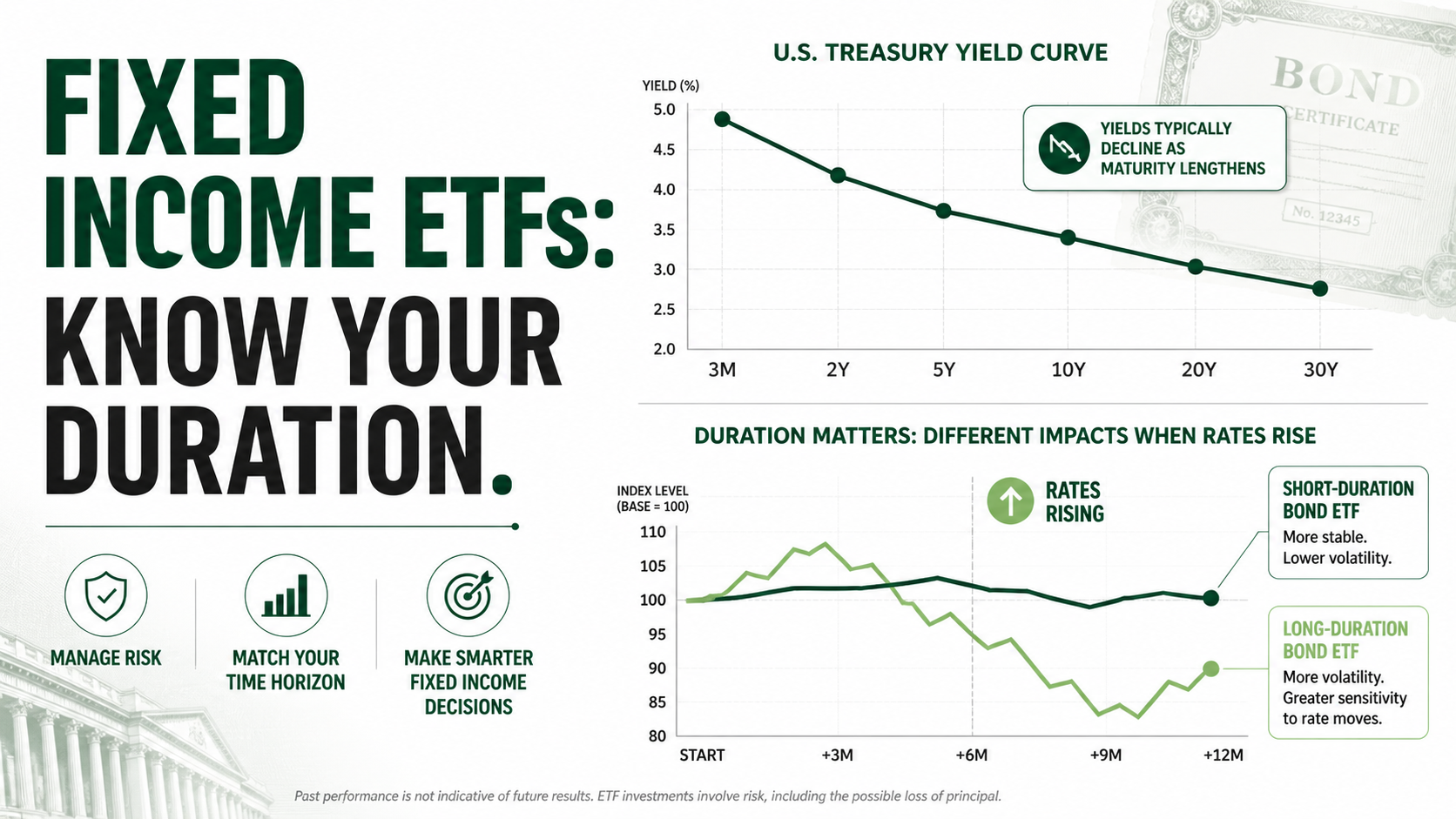

Duration and Interest Rate Risk: The Most Important Concept in Bond ETF Investing

| Duration Defined

Duration measures a bond ETF’s sensitivity to interest rate changes. A fund with a 5-year duration will lose approximately 5% in value for every 1% rise in interest rates — and gain approximately 5% for every 1% decline. The longer the duration, the greater the interest rate sensitivity in both directions. |

Duration is expressed in years — but it is not the same as maturity. A 10-year maturity bond has a duration of less than 10 years because it pays coupons along the way that return capital earlier than the final maturity date. Zero-coupon bonds have duration equal to maturity.

The inverse relationship between interest rates and bond prices is the core mechanic every fixed income ETF investor must internalize: when rates rise, existing bond prices fall. When rates fall, bond prices rise. Duration quantifies exactly how much.

Duration Sensitivity: A Practical Reference Table

| ETF Duration Category | Approx. Duration | Est. Price Change per 1% Rate Rise | Est. Price Change per 1% Rate Fall |

|---|---|---|---|

| Short-term (e.g. SHY) | ~2 years | ~-2% | ~+2% |

| Intermediate (e.g. BND, AGG) | ~6 years | ~-6% | ~+6% |

| Long-term (e.g. TLT) | ~17 years | ~-17% | ~+17% |

Price change estimates are approximations based on modified duration math. Actual fund responses depend on the specific yield level, convexity, and portfolio composition. Use fund fact sheets for precise duration figures.

The TLT 2022 Lesson

In 2022, the Federal Reserve raised interest rates by 425 basis points over the course of the year — the fastest rate-hiking cycle in four decades. TLT, the iShares 20+ Year Treasury ETF with approximately 17-year duration, fell approximately 30% peak-to-trough. Investors who held TLT as a ‘safe’ bond allocation experienced equity-level drawdowns in a fund composed entirely of U.S. government debt.

The 2022 experience was not a failure of bond ETFs — it was a lesson in the importance of duration selection. Short-duration Treasury ETFs (SHY, VGSH) fell approximately 4-5% during the same period. The difference in outcome was entirely determined by duration, not credit quality.

Rising vs Falling Rate Environments

In a rising rate environment: favor short-duration ETFs that limit price sensitivity while still generating income above cash. Long-duration ETFs become a headwind.

In a falling rate environment: longer duration becomes an amplifier of positive price movement. TLT and VGLT become return enhancers when rates decline meaningfully.

In a flat or uncertain rate environment: intermediate-duration funds (BND, AGG) offer a balanced risk/return profile without committing strongly to either direction.

The Best Fixed Income ETFs by Category

| Data Note

All expense ratios and fund details are illustrative approximations. Verify current figures at fund provider websites (Vanguard.com, iShares.com, Schwab.com, SSgA.com) before investing. |

The table below covers the most widely used fixed income ETFs across every major category. These are not obscure funds — they represent the industry-leading vehicles with the largest AUM, tightest bid-ask spreads, and lowest costs in their respective categories.

| Fund Name | Ticker | Category | Exp. Ratio | Approx. Duration | Best Use Case |

|---|---|---|---|---|---|

| Vanguard Total Bond Market ETF | BND | Broad Market | ~0.03% | ~6 yrs | Core bond allocation |

| iShares Core U.S. Agg Bond ETF | AGG | Broad Market | ~0.03% | ~6 yrs | Core bond — BND alternative |

| iShares 1-3yr Treasury Bond ETF | SHY | Short Gov. | ~0.15% | ~2 yrs | Rising rate stability |

| Vanguard Short-Term Treasury ETF | VGSH | Short Gov. | ~0.04% | ~2 yrs | Low-cost short-duration |

| iShares 20+ Year Treasury ETF | TLT | Long Gov. | ~0.15% | ~17 yrs | Falling rate / flight to quality |

| Vanguard Long-Term Treasury ETF | VGLT | Long Gov. | ~0.04% | ~17 yrs | Low-cost long duration |

| Vanguard Intermed. Corp Bond ETF | VCIT | Investment-Grade Corp. | ~0.04% | ~6 yrs | Higher yield vs Treasuries |

| iShares iBoxx IG Corporate ETF | LQD | Investment-Grade Corp. | ~0.14% | ~8 yrs | Broad IG corporate |

| iShares High Yield Corporate ETF | HYG | High-Yield | ~0.49% | ~4 yrs | Income-seekers / risk tolerance |

| iShares National Muni Bond ETF | MUB | Municipal | ~0.05% | ~6 yrs | High-bracket tax efficiency |

| Vanguard Short-Term TIPS ETF | VTIP | TIPS | ~0.04% | ~3 yrs | Inflation protection |

| iShares TIPS Bond ETF | TIP | TIPS | ~0.19% | ~7 yrs | Longer-duration inflation hedge |

BND vs AGG: Does the Choice Matter?

BND and AGG are functionally near-identical: both track U.S. investment-grade bond market indices, charge 0.03%, carry approximately 6-year duration, and provide broad diversification across government and corporate bonds. The choice between them is primarily a matter of brokerage preference — Vanguard account holders may prefer BND; iShares users may prefer AGG. At this level of similarity, the decision is not material.

The Municipal Bond Tax Calculation

Municipal bond ETFs like MUB offer lower pre-tax yields than comparable taxable bond ETFs. The comparison that matters is after-tax. To calculate taxable-equivalent yield: divide the municipal yield by (1 – your marginal tax rate). A 3.0% MUB yield for an investor in the 32% federal bracket is equivalent to a 4.41% taxable yield. At 37% it is equivalent to 4.76%. Always run this calculation before dismissing municipal bonds as lower-yielding.

Fixed Income ETFs vs Individual Bonds vs Stock ETFs

Bond ETF vs Individual Bond: What You Gain and Give Up

Owning an individual bond provides certainty that competing bond ETFs cannot match: if you hold to maturity, you receive your principal back at face value regardless of what interest rates do in the interim. This ‘maturity certainty’ is the primary reason some investors prefer individual bonds for laddering strategies — building a portfolio of bonds maturing at regular intervals.

The trade-off: individual bond portfolios require significantly larger capital (typically $100,000+) for meaningful diversification, carry the illiquidity of smaller markets, and require active monitoring of credit quality. Bond ETFs solve all three problems — but at the cost of the maturity certainty that makes individual bonds predictable.

Bond ETFs vs Stock ETFs: The Diversification Case (and Its Limits)

The traditional case for holding both stock and bond ETFs in a portfolio rests on their historically negative or low correlation: when equities fall, bonds typically rise as investors flee to safety, partially offsetting equity losses. This correlation held reliably from the early 2000s through 2021.

The 2022 exception: in 2022, the combination of an inflation shock and the Fed’s aggressive rate-hiking response caused both equities and long-duration bonds to fall simultaneously — the worst year for the 60/40 portfolio in decades. The lesson is not that bond ETFs no longer diversify, but that duration matters: short-duration bond ETFs performed far better than long-duration ones, and TIPS outperformed nominal bonds. The correlation between bonds and stocks is not constant — it is regime-dependent.

Tax Treatment: An Important Difference

Bond ETF income is taxed as ordinary income — at your marginal income tax rate, not the lower long-term capital gains rate. This makes bond ETFs less tax-efficient than equity ETFs in taxable accounts. Municipal bond ETFs offer federal tax exemption on interest income, addressing this disadvantage for investors in higher tax brackets. For tax-advantaged accounts (IRA, 401k), the tax treatment of bond income is deferred or eliminated — making these accounts the preferred location for taxable bond ETF holdings.

How Fixed Income ETFs Fit Into a Complete Portfolio

Fixed income ETFs serve three distinct functions in a complete portfolio, and understanding which function you need determines which type of fund belongs in your allocation.

- Income generation: regular monthly distributions from bond interest — relevant for investors seeking cash flow from their portfolio, particularly in retirement or income-focused strategies.

- Volatility reduction: the historically low or negative correlation between investment-grade bonds and equities reduces overall portfolio swings — the fundamental diversification benefit.

- Capital preservation: short-duration government bond ETFs protect capital during equity downturns and provide a stable foundation when equity volatility is elevated.

Duration Positioning by Rate Environment

The appropriate fixed income ETF depends partly on where you believe interest rates are heading — or, if you have no rate view, on your tolerance for price volatility.

Rising rates: short-duration ETFs (SHY, VGSH, VTIP) minimise price sensitivity. Sacrifice some yield for stability. BND and AGG are acceptable middle-ground choices.

Falling rates: longer-duration ETFs become return amplifiers. TLT and VGLT benefit most from meaningful rate declines. Only appropriate if you have a clear view or are using them tactically.

Uncertain / neutral: intermediate-duration broad market ETFs (BND, AGG) offer balanced exposure without committing to a rate direction. These work as the ‘default’ core bond allocation for most portfolios.

The Core/Satellite Framework for Fixed Income

ATGL’s recommended approach for most investors: use a broad-market intermediate-duration ETF (BND or AGG) as the core fixed income allocation — the stable foundation. Layer shorter or longer duration ETFs as satellite positions depending on your current rate view, income needs, or hedging objectives. Use TIPS ETFs when inflation risk is elevated. Consider municipal bond ETFs in taxable accounts if your marginal tax bracket is 22% or higher.

Active Investors: Bond ETFs as Strategic Tools

For active traders maintaining a parallel long-term portfolio, bond ETFs offer tactical versatility. TLT behaves as a meaningful equity hedge during flight-to-quality events — buying TLT during equity market stress has historically cushioned portfolio drawdowns. Short-duration government ETFs provide a liquid parking spot for capital between active equity positions. Understanding how different bond ETFs behave across rate cycles makes them a genuine multi-purpose tool rather than just a defensive afterthought.

Fixed Income ETFs Done Right

Fixed income ETFs are not interchangeable. Buying the wrong duration at the wrong time in the rate cycle produces outcomes that surprise investors who thought they owned something safe. Getting it right means knowing your duration, matching it to your rate view and risk tolerance, and treating each category — government, corporate, municipal, TIPS, high-yield — as a distinct tool with a specific role.

The selection framework in brief:

- Know the duration of any bond ETF before buying — it determines price risk, not just time horizon

- Match duration to rate environment: short in rising rates, long in falling rates, intermediate when uncertain

- Use municipal ETFs in taxable accounts if you’re in the 22%+ tax bracket — calculate taxable-equivalent yield

- Treat high-yield ETFs as equity-correlated; they don’t provide the diversification of investment-grade bonds

- BND and AGG are functionally equivalent — use whichever your brokerage makes commission-free

Building and managing a complete portfolio — across equity ETFs, sector funds, country ETFs, and fixed income — with consistent discipline and a clear allocation framework is exactly what ATGL’s system is designed to help you do.

| Build Your Complete ETF Portfolio With ATGL

At AboveTheGreenLine.com we give investors the analytical framework to evaluate, select, and manage every ETF category with the same disciplined, rules-based approach. From equity strategies to fixed income allocation, join us Above the Green Line and get access to the complete system. |

Frequently Asked Questions

Are fixed income ETFs safe?

Fixed income ETFs are generally lower risk than equity ETFs but are not risk-free. Government bond ETFs carry minimal credit risk but significant interest rate risk — particularly long-duration funds like TLT. High-yield ETFs carry both credit risk and behave like equities during market stress. The primary risks across all fixed income ETFs are interest rate risk (bond prices fall when rates rise), credit risk, and inflation risk.

What is the difference between a bond ETF and a bond fund?

Bond ETFs and bond mutual funds both hold portfolios of bonds, but bond ETFs trade on exchanges throughout the day at market prices, while bond mutual funds are priced once daily at NAV. Bond ETFs generally have lower expense ratios, no investment minimums, and slightly better tax efficiency through in-kind redemption mechanisms that typically avoid capital gains distributions.

How do fixed income ETFs pay income?

Fixed income ETFs collect coupon interest payments from the bonds they hold and distribute this income to shareholders, typically monthly. The distribution amount fluctuates over time as the portfolio is rebalanced — when older bonds mature and are replaced by new bonds at prevailing market yields, the income profile shifts. Unlike individual bonds with a fixed coupon, bond ETF income adapts to the current interest rate environment.

What happens to bond ETFs when interest rates rise?

When interest rates rise, bond prices fall — and bond ETF prices fall with them. The magnitude depends on duration: TLT (17-year duration) fell approximately 30% during the 2022 rate-hiking cycle; SHY (2-year duration) fell approximately 4-5% over the same period. Short-duration ETFs are most resilient in rising rate environments; long-duration ETFs suffer the largest price declines but gain the most when rates eventually fall.

Related Articles

[pt_view id=”fb2451fm3r”]