By Andrew Stowers

Updated May 19, 2026

Money market funds are one of the most widely used financial instruments in the world — collectively holding trillions of dollars in assets — yet they are routinely confused with something entirely different: money market accounts.

They share a name but are legally, structurally, and practically distinct. This guide explains exactly what money market funds are, how the three main types differ, how to evaluate them using the right metrics, how they compare to their exchange-traded equivalents — and for active investors — why they are the right vehicle for managing dry powder between positions. After reading this guide, we encourage you to review our ETF Investing Guide to see how this all fits into the bigger picture.

What Is a Money Market Fund? (And How It Actually Works)

| Quick Answer

A money market fund is a type of mutual fund that invests in short-term, high-quality debt instruments — primarily U.S. Treasury bills, commercial paper, certificates of deposit, and repurchase agreements — and aims to maintain a stable $1.00 net asset value (NAV) per share. Money market funds are regulated by the SEC under Rule 2a-7 and are NOT FDIC-insured. |

The $1.00 NAV is the defining convention of money market funds: each share is intended to be worth exactly one dollar at all times. This convention is maintained by investing only in short-term, high-credit-quality securities whose market prices fluctuate very little. It is a goal and a strong historical norm — not a legal guarantee.

What Money Market Funds Invest In

The specific instruments vary by fund type but generally include: U.S. Treasury bills (short-term government debt maturing in one year or less), U.S. agency and government-sponsored enterprise securities, repurchase agreements backed by government securities, commercial paper (short-term corporate promissory notes — in prime funds), certificates of deposit, and short-term municipal debt.

How Your Income Is Generated and Distributed

As the fund collects interest on its short-term holdings, that income accrues to shareholders on a daily basis. Most money market funds distribute this accumulated income monthly as dividends. Your balance grows each day — invisibly, without share price changes — and a consolidated income distribution appears in your account monthly. This daily accrual / monthly distribution mechanic means your money is working every day, not just on distribution dates.

The Regulatory Framework: SEC Rule 2a-7

Money market funds are regulated under the SEC’s Rule 2a-7, which imposes strict requirements on four dimensions: portfolio quality (only investment-grade securities), maturity limits (weighted average maturity capped at 60 days, weighted average life capped at 120 days), diversification (no single issuer can exceed 5% of the portfolio, with government securities exempt), and liquidity (government funds must hold at least 50% in daily liquid assets). These requirements are the primary reason money market funds are among the safest mutual fund structures available.

Money Market Funds vs Money Market Accounts: A Critical Distinction

| The Most Common Confusion

Money market funds and money market accounts share a name but are entirely different financial products. A money market fund is a mutual fund — not FDIC-insured, not a deposit account. A money market account is a deposit account at a bank — FDIC-insured up to $250,000, guaranteed principal, typically lower yield. These are not interchangeable. |

The confusion between these two products is understandable and widespread. Both offer liquidity, both are associated with conservative cash management, and both often carry competitive short-term interest rates. But the differences are significant and consequential.

| Feature | Money Market Fund | Money Market Account |

|---|---|---|

| Product Type | Mutual fund (SEC-regulated) | Bank deposit account (FDIC/NCUA) |

| FDIC Insurance | NOT insured | Insured up to $250,000 |

| Principal Guarantee | No (though $1.00 NAV is stable) | Yes — guaranteed by FDIC |

| Typical Yield | Competitive — tracks Fed funds rate | Often lower; set by the bank |

| Where It’s Held | Brokerage account | Bank or credit union |

| Transaction Limits | None (for most broker platforms) | Federal limits may apply |

| State Tax on Interest | Often exempt (government funds) | Fully taxable |

When to Choose Each

Choose a money market account when: capital you absolutely cannot afford to lose, amounts under $250,000 where FDIC guarantee matters most, or as the core of a truly risk-free emergency fund.

Choose a money market fund when: capital held at a brokerage, amounts above the $250,000 FDIC limit, seeking higher yield with competitive rates, or as the default vehicle for idle brokerage cash. For active investors, the brokerage-based money market fund is almost always the appropriate vehicle.

For deeper context on the safety of money market accounts specifically, see ATGL’s dedicated analysis.

The Three Types of Money Market Funds

Not all money market funds are the same. The three main types differ in what they hold, their risk profile, their yield potential, and their tax treatment — and choosing the right type for your situation matters.

| Type | Holdings | Stable $1 NAV | Credit Risk | State Tax | Best For |

|---|---|---|---|---|---|

| Government / Treasury | T-bills, agency debt, repos | Yes (retail) | Minimal | Exempt | Safety-first investors |

| Prime | Corp. commercial paper, bank CDs | Yes (retail) | Low but real | Taxable | Higher yield seekers |

| Tax-Exempt | Short-term municipal debt | Yes (retail) | Very low | Fed exempt | High tax bracket investors |

Government / Treasury Money Market Funds

Government money market funds invest exclusively in U.S. Treasury securities (bills, notes, and bonds with remaining maturities under 397 days) and repurchase agreements backed by U.S. government securities. They carry the lowest credit risk of any money market fund type — the full faith and credit of the U.S. government backs the underlying securities. Critically, interest income is generally exempt from state and local income taxes, providing an after-tax yield advantage for investors in high-tax states.

Well-known examples include VMFXX (Vanguard Federal Money Market Fund), SPAXX and FDRXX (Fidelity Government Money Market funds), and SWVXX (Schwab Value Advantage Money Market Fund). Verify current yields and expense ratios at each fund’s provider website — these change daily.

Prime Money Market Funds

Prime funds invest in a broader range of short-term instruments: corporate commercial paper, bank certificates of deposit, and other non-government debt alongside government securities. This broader mandate allows prime funds to capture a modest yield premium over government-only funds — typically 0.05–0.20% in normal market environments.

Important regulatory note: the 2016 SEC money market fund reform required institutional prime and tax-exempt funds to use a floating NAV (rather than stable $1.00). This change caused substantial capital to migrate from institutional prime funds to government funds. Retail prime funds (the ones available to individual investors at standard brokerages) retained the stable $1.00 NAV convention. However, prime funds may impose liquidity fees or redemption gates during periods of market stress — a restriction government funds do not face.

Tax-Exempt Money Market Funds

Tax-exempt funds invest in short-term municipal debt — securities issued by state and local governments. The interest income is exempt from federal income tax and may be exempt from state income tax for in-state securities. The pre-tax yield is lower than government or prime funds, but the after-tax yield can be competitive for investors in the 22% or higher federal tax bracket. Calculate taxable-equivalent yield (fund yield divided by (1 minus your marginal tax rate)) to make a valid comparison.

Key Metrics: How to Evaluate Any Money Market Fund

Choosing between money market funds requires understanding five specific metrics. Knowing these allows you to evaluate any fund independently — rather than accepting your brokerage’s default or highest-advertised option without scrutiny.

1. 7-Day Yield

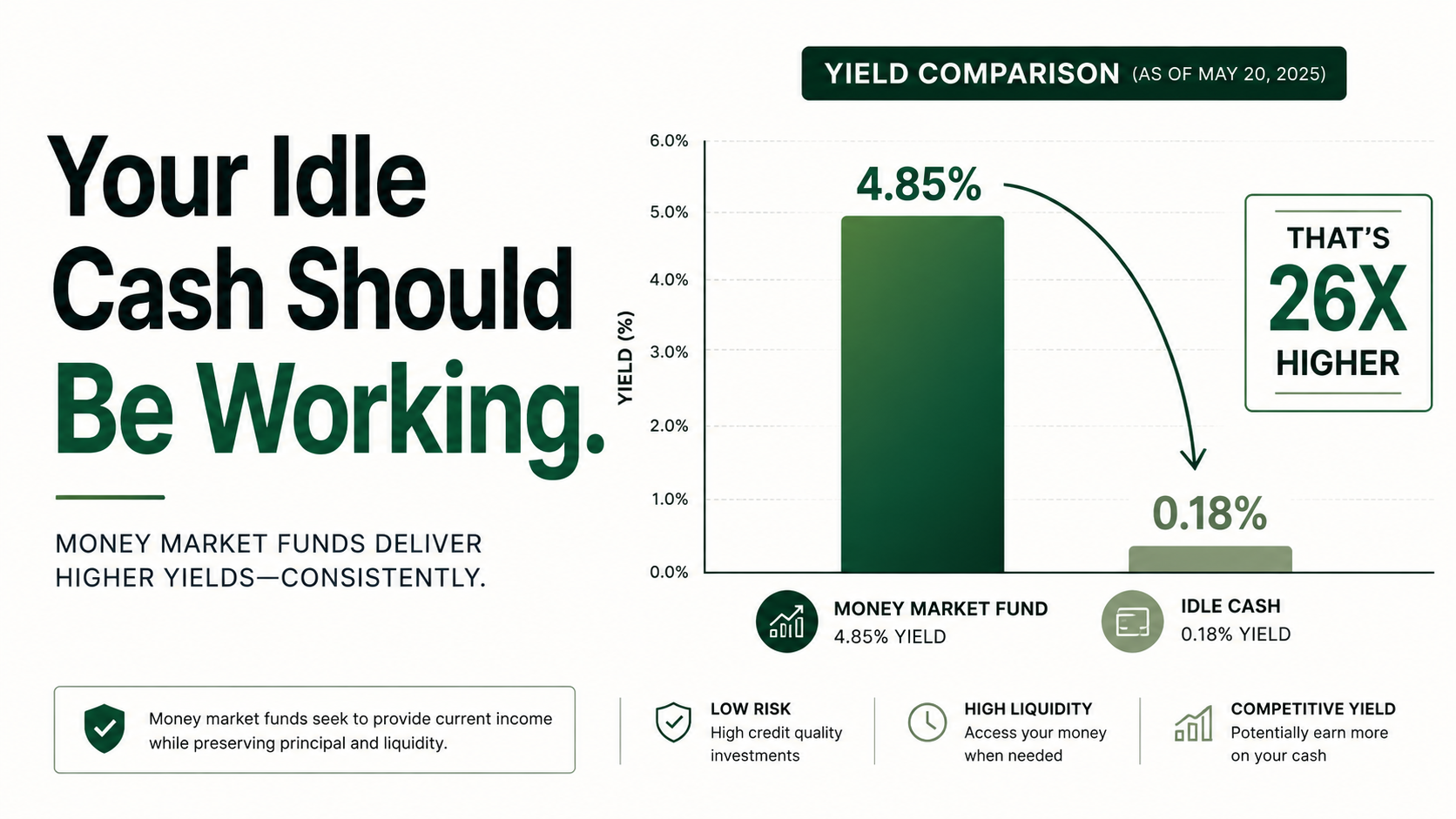

The 7-day yield is the standard performance metric for money market funds. It annualizes the income earned over the most recent seven calendar days, reflecting current market conditions more accurately than longer-period metrics. When comparing funds, always compare 7-day yields — and check them at the fund provider’s website, where they are updated daily. A fund yielding 4.85% today may yield 4.70% next week if conditions change.

2. Expense Ratio

The expense ratio is deducted from the fund’s gross yield before income reaches you. A fund generating 5.00% gross with a 0.11% expense ratio delivers approximately 4.89% to investors. Vanguard, Fidelity, and Schwab typically offer the most competitive expense ratios in the category — often in the 0.01%–0.12% range for their flagship government funds. Higher expense ratios at competing providers or older share classes can meaningfully reduce net yield on otherwise similar funds.

3. Weighted Average Maturity (WAM)

WAM measures the average time until the holdings in the fund mature. SEC Rule 2a-7 caps WAM at 60 days for all money market funds. A fund with a very short WAM (10–20 days) will adjust its yield more rapidly when the Federal Reserve changes rates — the portfolio rolls over quickly into new securities at current rates. A fund near the 60-day cap will lag in adjusting. In a rate-cutting environment, a shorter WAM means your yield declines faster; in a rate-hiking environment, a shorter WAM means you capture higher rates sooner.

4. Weighted Average Life (WAL)

WAL extends WAM by accounting for the final legal maturity of securities rather than their reset dates. Rule 2a-7 caps WAL at 120 days. While less commonly watched than WAM, WAL provides additional insight into the fund’s exposure to longer-dated paper that might have short-term rate resets but longer legal maturities.

5. Daily and Weekly Liquidity Ratios

SEC rules require government money market funds to hold at least 50% of assets in daily liquid assets (securities maturing in one business day or overnight repos). Higher liquidity ratios mean the fund has more flexibility to meet heavy redemption demand without disrupting remaining holdings. In normal markets this rarely matters; in stress events it becomes critical.

Top Money Market Funds and Their Treasury ETF Alternatives

| Data Note

All yields change daily with market conditions. Verify current 7-day yields and expense ratios at Vanguard.com, Fidelity.com, Schwab.com, iShares.com, and SSgA.com before making any investment decision. |

Top Money Market Funds

The most widely available government money market funds at the major U.S. brokerages — covering the options most readers will actually encounter:

| Fund Name | Ticker | Available At | Type | Approx. ER | Verify Yield |

|---|---|---|---|---|---|

| Vanguard Federal Money Market | VMFXX | Vanguard | Government | ~0.11% | Vanguard.com |

| Fidelity Government Money Market | SPAXX | Fidelity | Government | ~0.42% | Fidelity.com |

| Fidelity Money Market (Premium) | FDRXX | Fidelity | Government | ~0.12% | Fidelity.com |

| Schwab Value Advantage Money Mkt | SWVXX | Schwab | Prime | ~0.34% | Schwab.com |

| Schwab Government Money Market | SNVXX | Schwab | Government | ~0.34% | Schwab.com |

Note: fund availability, expense ratios, and minimum investment requirements vary by brokerage platform and share class. Verify all details at fund provider websites.

Treasury ETF Alternatives: The Exchange-Traded Option

For investors who want the near-equivalent of a government money market fund in an exchange-traded format — tradeable intraday at any brokerage, with no fund-specific minimums — Treasury bill ETFs are the most direct alternative:

| ETF Name | Ticker | Index / Focus | Approx. ER | Key Feature |

|---|---|---|---|---|

| iShares 0-3 Month Treasury Bond | SGOV | ICE 0-3 Month T-Bill Index | ~0.09% | Lowest ER; near-identical to MMF |

| SPDR Bloomberg 1-3 Mo T-Bill | BIL | Bloomberg 1-3 Month T-Bill | ~0.136% | Oldest, highest AUM T-bill ETF |

| WisdomTree Floating Rate Treasury | USFR | Bloomberg 3-Month SOFR-like | ~0.15% | Adjusts quickly with rate changes |

Money Market Fund vs Treasury ETF: When Each Is Better

Choose a money market fund when: you are at a major brokerage (Vanguard, Fidelity, Schwab) where the fund is easily accessible, you want the stable $1.00 NAV convention for accounting simplicity, the fund is your brokerage’s default cash sweep, or you prefer monthly income distributions over variable ETF distributions.

Choose a Treasury ETF (SGOV, BIL) when: you need intraday tradability — the ability to sell and receive proceeds within the same trading session for immediate redeployment, you hold accounts at brokerages with less competitive money market fund options, or you want the ability to transact in any brokerage account without fund-specific access requirements.

Risks Every Money Market Fund Investor Must Understand

Money market funds are among the safest non-deposit investment instruments available — but they are not risk-free. Three specific risks deserve clear understanding.

Risk 1: Breaking the Buck

‘Breaking the buck’ refers to a money market fund’s NAV falling below $1.00 per share — turning what investors expect to be a stable-value instrument into one with a loss. In modern U.S. money market fund history, this has occurred once with a widely-held retail fund.

In September 2008, the Reserve Primary Fund — then one of the largest money market funds in the world — held approximately $785 million in commercial paper issued by Lehman Brothers. When Lehman filed for bankruptcy, those securities became effectively worthless. The fund’s NAV fell to $0.97 per share. The event triggered a broader money market run that required government intervention to stabilize.

Government-only money market funds have never broken the buck. Because they hold exclusively U.S. government-backed securities, their holdings cannot default. The breaking-the-buck risk is specific to prime funds holding corporate paper — and the 2016 SEC reforms, which imposed floating NAVs on institutional prime funds and liquidity tools, were designed to reduce the systemic risk this creates.

Risk 2: Yield Risk (Not Price Risk)

The most common risk for money market fund holders is yield risk — the income return changes when the Federal Reserve changes interest rates. In a rate-cutting cycle, money market fund yields decline proportionally with the Fed funds rate. This is different from price risk: your $1.00 NAV is maintained, but you earn less income on it.

For active traders and investors using money market funds to park capital, this is an important dynamic to track: when the Fed signals rate cuts, the attractiveness of money market funds relative to slightly longer-duration instruments declines. Migrating some capital to short-duration bond ETFs may capture better yield before rates fall.

Risk 3: Credit Risk in Prime Funds

Prime money market funds hold corporate commercial paper and bank certificates of deposit alongside government securities. These instruments carry real, if small, credit risk — the possibility that an issuing corporation or bank cannot repay its short-term obligations. This risk is managed by diversification requirements, credit quality standards, and the short-term nature of the holdings, but it is not zero. The 2008 Reserve Primary Fund event was a manifestation of this exact risk.

How Money Market Funds Fit Into an Active Investor’s Strategy

| The Opportunity Most Active Investors Miss

An active investor with $50,000 in uninvested capital earns approximately $2,250 per year by parking it in a government money market fund at 4.5% — compared to effectively nothing in a non-interest-bearing default cash balance. Over a full year with multiple position cycles, idle capital yield can be a meaningful contributor to total portfolio return. |

The Dry Powder Concept

Active traders typically hold meaningful portions of their portfolio in cash at any given time — waiting for the right setup, between positions, or preserving capital during high-volatility periods. Depending on trading style and market conditions, this dry powder can represent 15–40% of total capital. Leaving it in a non-interest-bearing cash balance is a passive decision that costs real money in a higher-rate environment.

Government money market funds and Treasury bill ETFs (SGOV, BIL) capture yield on that capital without sacrificing the liquidity needed to deploy it quickly when opportunities arise. The trade-off — fractionally less immediate liquidity versus a savings account — is negligible for most active trading strategies.

Money Market Fund vs Treasury ETF for Deployment Speed

The key practical distinction for active traders: Treasury bill ETFs offer same-session liquidity. If a setup appears at 10 AM, you can sell SGOV at 10:05 AM and use the proceeds to buy a stock at 10:10 AM in the same trading session. Money market fund redemptions may take until the next business day to settle, depending on the fund and brokerage. For fast-moving active traders, SGOV or BIL’s intraday liquidity can be materially useful.

The Cash Sweep Default: Know What Your Brokerage Is Paying You

Most brokerages automatically sweep idle cash into a default money market fund or cash equivalent. The critical point: the default sweep vehicle at your brokerage may offer a significantly lower yield than alternative money market funds available at the same institution.

Some brokerages default idle cash into bank sweep programs earning well below 1% while simultaneously offering government money market funds yielding 4-5%. The difference is not disclosed prominently — but it is real, it is substantial, and it represents an easy, fee-free improvement for any investor who checks and acts.

Tax Efficiency in Taxable Accounts

For investors in high tax brackets (32%+) holding money market funds in taxable brokerage accounts, the state and local tax exemption on government fund dividends provides a meaningful after-tax yield advantage over equivalent bank products. Factor this into your comparison when evaluating money market funds against high-yield savings accounts for non-retirement capital.

Make Every Dollar Work — Including the Ones Between Trades

Money market funds are not glamorous — they are quietly one of the most useful instruments in an investor’s toolkit. For passive investors, they provide safe, competitive short-term yield on capital waiting to be deployed or held for income. For active traders, they are the right vehicle for capturing return on dry powder that would otherwise sit idle.

The selection framework in brief:

- Government money market funds — VMFXX, SPAXX, SWVXX — for safety-first investors at major brokerages

- Treasury ETFs — SGOV, BIL — for active traders needing intraday liquidity or investors at brokerages with less competitive fund options

- Tax-exempt funds for investors in the 22%+ federal bracket holding capital in taxable accounts

- Always check your brokerage’s default sweep rate — and upgrade if better options are available at the same institution

Managing every dollar in your portfolio intelligently — not just the dollars in active positions — is part of what separates disciplined investors from undisciplined ones. Idle capital should earn something.

| Build a Complete Portfolio System With ATGL

At AboveTheGreenLine.com we give investors the complete framework for every capital allocation decision — from where to park idle cash to how to build and manage active trading positions. Every dollar has a job. Join us Above the Green Line and get the system that makes sure it does one. |

Frequently Asked Questions

Is a money market fund the same as a savings account?

No. A money market fund is a mutual fund — it is not a bank account, is not FDIC-insured, and invests in short-term debt securities. A savings account is a deposit account at a bank, FDIC-insured up to $250,000. Money market funds typically offer competitive yields and high liquidity, but your principal is not federally guaranteed the way it is in a savings account. In a higher-rate environment, money market funds often offer meaningfully better yields.

Can you lose money in a money market fund?

Yes, though it is exceptionally rare for government money market funds. The risk is ‘breaking the buck’ — when the fund’s NAV falls below $1.00. This occurred once in modern history with the Reserve Primary Fund in September 2008, which held Lehman Brothers commercial paper that became worthless when Lehman filed for bankruptcy. Government-only money market funds, which hold exclusively U.S. government-backed securities, have never broken the buck.

What is a good money market fund yield?

Money market fund yields move directly with the Federal Reserve’s federal funds rate. In a 4-5% rate environment, top-tier government money market funds typically yield within 0.10-0.25% of the federal funds rate, net of their expense ratios. When the Fed cuts rates, money market yields decline proportionally. Check current 7-day yields at fund provider websites — they are updated daily and change with market conditions.

How are money market funds taxed?

Government money market fund dividends are generally exempt from state and local income taxes but taxable at the federal level — a meaningful advantage for investors in high-tax states. Prime money market fund dividends are taxable at both federal and state levels. Tax-exempt money market fund dividends are exempt from federal income tax. The state tax exemption on government funds can make them more attractive than equivalent yields from taxable instruments on an after-tax basis. Consult a tax professional for guidance specific to your situation.

Related Articles

[pt_view id=”fb2451fm3r”]