By Andrew Stowers

Updated April 28, 2026

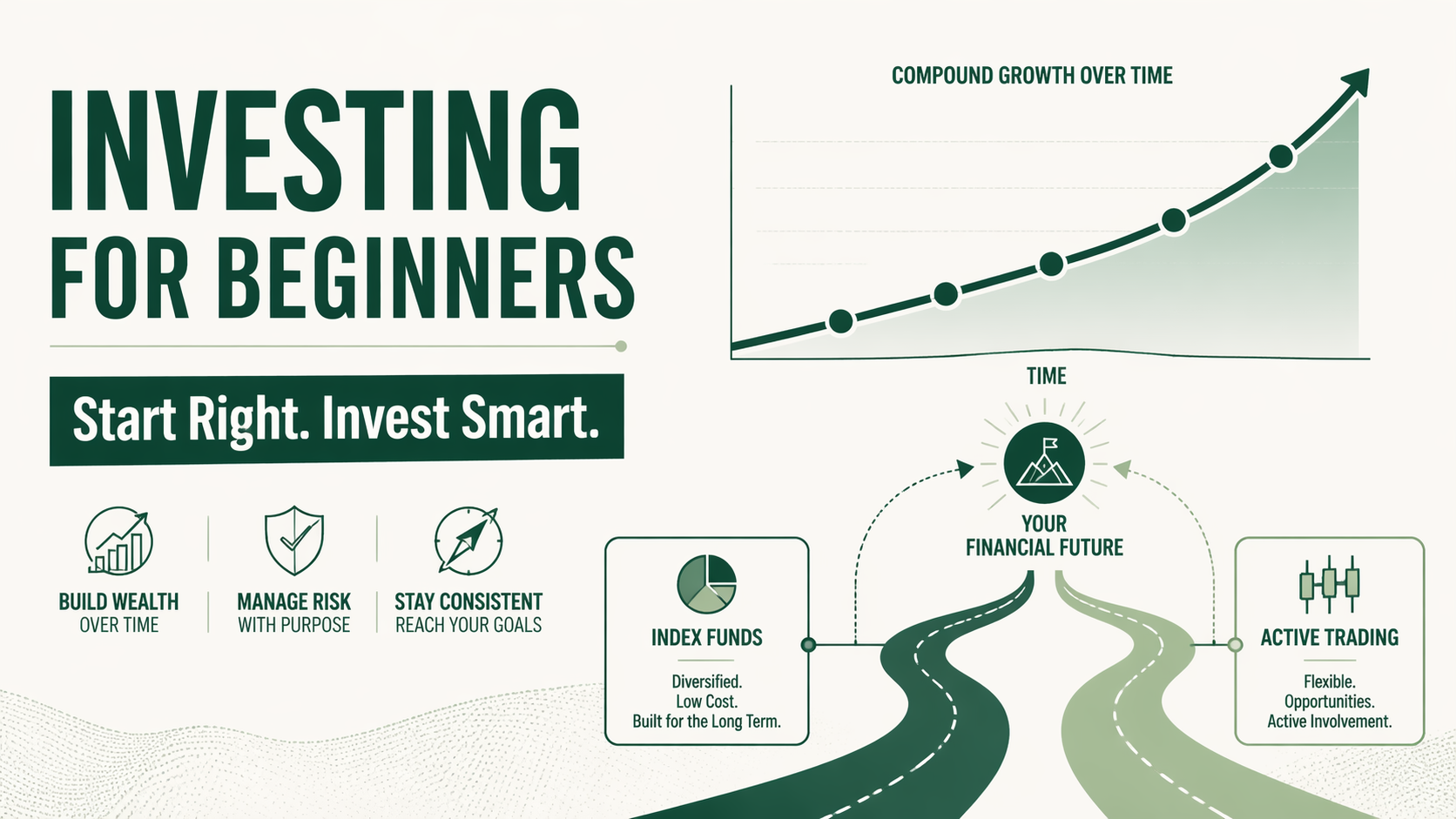

Most investing guides for beginners give you the same advice: open a brokerage account, buy an index fund, and wait 30 years. That advice is good — but it’s incomplete.

It tells you what to buy. It doesn’t tell you how to think, how to manage risk, or what to do if you want to be more than a passive spectator in your own financial future. And it assumes everyone wants the same thing, which they don’t.

Supplementing our Stock Trading Guide, this guide covers everything a new investor needs to actually get started with clarity: what investing is and why it beats saving over time, the fork in the road between passive and active approaches, what to buy, how to protect yourself from mistakes that end most beginners’ journeys in year one, and the mindset framework that separates investors who build real wealth from those who spin their wheels.

What Is Investing — and Why Does It Matter More Than Saving?

| Quick Answer

Investing means putting money into assets — stocks, ETFs, bonds, real estate — that can grow in value or generate income over time. Unlike saving, which preserves money at minimal return, investing accepts calculated risk in exchange for the potential to compound wealth significantly over years and decades. |

A savings account keeps your money safe and accessible. In 2026, the best high-yield savings accounts pay roughly 4–5% APY — which sounds reasonable until you account for inflation and the opportunity cost of capital sitting still.

The stock market, measured by broad indices like the S&P 500, has returned approximately 7–10% annually on average over long historical periods after inflation. That gap — between a savings account and a diversified market investment — is where wealth is built or lost.

The mathematics of compounding make this concrete. A single $10,000 investment at 8% annual return — with no additional contributions — grows to approximately $100,000 in 30 years. The same $10,000 in a 4% savings account grows to approximately $32,000 over the same period. The difference is not effort, timing, or luck. It is asset selection and time.

The important clarification: risk is not the enemy. Unmanaged risk is. Every asset class carries some form of risk — market risk, inflation risk, liquidity risk. The goal of investing is not to eliminate risk but to understand it, size positions appropriately, and ensure the potential reward justifies taking it.

Key Concepts Every Beginner Must Understand

Before investing a dollar, you need a working vocabulary. These six concepts are not advanced theory — they are the basic framework for making informed decisions.

Asset Classes

An asset class is a category of investment with similar characteristics and market behaviour. The four core asset classes are: equities (stocks — ownership in companies), fixed income (bonds — loans to governments or corporations that pay interest), cash and cash equivalents (money market funds, T-bills), and alternative assets (real estate, commodities, private equity). Each offers a different risk/return trade-off. A beginner’s portfolio will primarily involve equities and, over time, some fixed income.

Diversification

Diversification means spreading your capital across multiple assets, sectors, and geographies so that no single failure can devastate your portfolio. Owning one stock means your returns depend entirely on that company. Owning a broad-market ETF means your returns reflect thousands of companies — one failing has minimal impact. Diversification is the closest thing to a free lunch in investing.

Time Horizon

Your time horizon is how long you plan to leave money invested before needing it. A 25-year-old investing for retirement has a 40-year horizon and can absorb significant short-term volatility. A 55-year-old with a 10-year horizon needs a more conservative allocation. Time horizon is the single biggest determinant of how much risk is appropriate to take.

Liquidity

Liquidity is how quickly an asset can be converted to cash without significantly affecting its price. Stocks and ETFs listed on major exchanges are highly liquid — you can sell at any time during market hours. Real estate is illiquid — selling takes weeks to months. Beginners should prioritise liquid assets until they have a well-established emergency fund and clear investment plan.

Volatility

Volatility measures the range of price movement in an asset over time. A stock that moves 3% up or down in a day is more volatile than one that moves 0.3%. Higher volatility means larger potential gains and larger potential losses. Beginners often underestimate how emotionally difficult volatility is to sit through — building experience with smaller positions before scaling up is a sound approach.

Market Cycles

Markets move in cycles between bull markets (sustained uptrends, rising asset prices) and bear markets (sustained downtrends, 20%+ decline from peak). Understanding that both are normal parts of the cycle — and that bear markets are opportunities, not just losses — is foundational to the mindset every successful long-term investor must develop.

The Two Paths: Passive Investor or Active Trader?

| Quick Answer

Passive investing means buying diversified index funds or ETFs and holding them for years or decades — letting compound growth do the work with minimal intervention. Active trading means buying and selling based on strategy, analysis, and defined rules — seeking returns above the market benchmark. Both are legitimate; most serious investors use both. |

This is the fork in the road that most beginner guides completely ignore — and it matters enormously for how you structure your time, capital, and learning.

Path 1: Passive Investing

Passive investors buy diversified ETFs or index funds and hold them for years or decades. Their goal is to capture the long-term growth of the market at minimal cost. The evidence supports this approach strongly: over 15–20 year periods, the vast majority of actively managed funds underperform their benchmark index after fees.

Passive investing requires minimal time, no stock-picking skill, and is emotionally manageable for most people — because there are no decisions to make once you’ve chosen your funds. It is the right primary approach for the majority of your capital throughout your investing life.

Path 2: Active Trading

Active traders buy and sell individual stocks, ETFs, or other instruments based on a defined strategy — whether that’s technical analysis, fundamental analysis, Swing Trading, or a combination. The goal is to generate returns above the market benchmark.

Active trading requires time, skill development, emotional discipline, and — critically — a rules-based system that removes as many emotional decisions as possible. It is not gambling if done correctly. But most people who attempt it without a systematic approach do underperform the market, and many lose money.

The Hybrid Approach: Core + Satellite

The approach most ATGL members use — and the one that makes the most practical sense — is to treat these paths not as opposing choices but as complementary layers. The core of your portfolio (60–80% of invested assets) sits in low-cost passive index funds. The satellite (20–40%) is deployed in active strategies where you have an edge, time to manage positions, and a clear rules-based framework.

This structure keeps the bulk of your capital compounding efficiently at low cost, while giving you the opportunity to develop active trading skills and generate alpha with the portion you actively manage.

What Should a Beginner Actually Buy?

| Quick Answer

For most beginners, the best first investment is a low-cost broad-market ETF or Index Fund — such as a total U.S. market fund or S&P 500 fund. It provides instant diversification, charges minimal fees (0.03–0.05%), and tracks the overall market without requiring stock-picking skill. |

Here is a comparison of the main investment vehicles available to beginners, with a clear-eyed view of what each is suited for.

| Vehicle | Risk Level | Time Horizon | Best For | Example |

|---|---|---|---|---|

| Broad-market ETF | Low–Moderate | Long (5+ yrs) | Core diversified holding | VTI, ITOT |

| S&P 500 Index Fund | Low–Moderate | Long (5+ yrs) | U.S. large-cap exposure | VOO, IVV, FXAIX |

| International ETF | Moderate | Long (5+ yrs) | Geographic diversification | VXUS, SWISX |

| Individual Stocks | Moderate–High | Medium–Long | Higher conviction picks | Varies |

| Bond ETF | Low–Moderate | Medium–Long | Income, capital preservation | BND, SCHZ |

| Cash Equivalents | Very Low | Short | Emergency fund, short-term savings | SGOV, VMFXX |

Tickers above are illustrative examples only. Verify current expense ratios and holdings at fund provider websites before investing.

The Practical Starting Recommendation

For a beginner’s first investment, a broad-market U.S. ETF or total market index fund is the right starting point. It gives you immediate exposure to thousands of companies across every sector, charges a minimal fee (0.03–0.05% annually), and requires no stock-picking decisions.

Once you have that foundation in place — even if it starts at $500 — you can expand incrementally: add international exposure, consider a bond allocation based on your time horizon, and begin researching individual stocks or sector ETFs if you want to develop active skills alongside your passive core.

The question is never which is the perfect first investment. The question is whether you have started. Time in the market is the most powerful variable in compounding — and every month you delay starting is a month of compounding you cannot get back.

Risk Management: The Skill That Determines Who Survives

Most beginner investing guides cover what to buy. Almost none cover how to manage the risk of what you buy. This is the gap that causes most new investors to blow up in year one — not bad stock picks, but bad risk management.

Risk management is not an advanced topic. It is the most important skill a beginner can develop, and the three fundamentals below can be understood and applied immediately.

1. Position Sizing

Position sizing determines how much capital you allocate to any single investment. The most commonly cited starting rule is the 1–2% rule: never risk more than 1–2% of your total portfolio on any single trade or position.

In practical terms: if you have $10,000 invested and you’re considering a stock position, your maximum acceptable loss on that position should be $100–$200. This means your position size depends on where you set your stop-loss. A stock you’re willing to hold through a 10% decline requires a smaller position than one you’d cut at 5%.

Position sizing is the mechanism that ensures a single bad trade cannot derail your overall portfolio. New investors consistently size positions too large — driven by conviction or excitement — and pay the price when those positions move against them.

2. Stop-Losses

A stop-loss is a pre-defined exit point — the price at which you will sell a position to limit your loss if the trade goes wrong. Setting a stop-loss before you enter a position is the difference between a disciplined trade with defined risk and an open-ended bet.

The purpose of a stop-loss is not to prevent all losses. Losses are part of investing. The purpose is to ensure that when you are wrong, you are wrong for a small, manageable, pre-determined amount — not for however much the stock falls before emotion forces you to act.

3. Risk/Reward Ratio

Before entering any position, define both your expected reward (the price target where you’ll take profits) and your accepted risk (the stop-loss where you’ll exit if wrong). The ratio of potential reward to potential risk is your risk/reward ratio.

A 2:1 risk/reward ratio means you’re risking $1 to make $2. If you maintain a consistent 2:1 R/R ratio and are right only 50% of the time, you still make money. This mathematics is the foundation of every sustainable trading strategy.

| ATGL Risk Framework

These three principles — position sizing, stop-losses, and risk/reward ratios — are not advanced concepts reserved for professional traders. They are the basic toolkit of any investor who wants to survive long enough to learn. Build these habits from your very first position. |

Your Practical First Steps: Opening an Account and Making Your First Investment

Theory without action is just reading. Here is the five-step framework to go from zero to your first investment.

- Choose your account type: A taxable brokerage account gives you full flexibility — deposit any amount, invest in anything, withdraw at any time. A tax-advantaged account (IRA, 401k) offers tax benefits but has annual contribution limits and withdrawal restrictions. Most beginners should open both: start with a Roth IRA if you qualify (contributions grow tax-free), and use a taxable account for capital above the IRA limit or that you may need sooner.

- Select a broker: The major platforms — Fidelity, Schwab, and Vanguard — all offer $0 account minimums, commission-free ETF trades, and strong educational resources. Any of the three is an excellent choice. Pick the one whose interface you find most intuitive and whose fund lineup matches your planned investment vehicles.

- Fund your account: Link your bank account and transfer your initial deposit. Start with whatever you can genuinely commit to leaving invested for your chosen time horizon. Even $100 gets you started. More importantly, set up a recurring monthly transfer — $50, $100, $200 — so investing becomes automatic rather than a decision you have to make each month.

- Make your first investment: Search for your chosen ETF or index fund by ticker, enter the number of shares or dollar amount, and use a limit order (not a market order) to control the exact price you pay. Review the order before confirming. Your first purchase does not have to be large — it just has to be made.

- Set up recurring contributions: Dollar-cost averaging — investing a fixed amount on a regular schedule regardless of market conditions — is the single most effective way to remove timing anxiety and build consistent investing discipline. Set it up as an automatic transfer and let it run.

The Beginner Mindset: Why Most People Fail (And How to Be Different)

Most beginners do not fail because they picked the wrong stock or chose the wrong ETF. They fail because of three mindset errors that are entirely preventable.

Emotional Decision-Making

The most reliable pattern in retail investor behavior is also the most costly: buying when excitement peaks (near market tops) and selling when fear peaks (near market bottoms). This cycle is not a character flaw — it is the natural human response to financial uncertainty. But acting on it consistently produces the opposite of the intended result.

The antidote is a plan made before the market moves, not in response to it. Decide your entry criteria, your position size, and your exit before you invest. When the market becomes volatile, your job is to execute the plan — not to improvise.

Overtrading

The illusion of control is powerful. Checking your portfolio 10 times a day, moving between positions every few weeks, reacting to every news headline — this feels like active management. It is not. It is expensive noise. Transaction costs, tax drag, and poor execution accumulate quietly but relentlessly.

The data is unambiguous: most active traders underperform the index they are trying to beat. Most of that underperformance is not from a single bad trade — it is from the accumulated cost of too much activity. Fewer, higher-conviction positions held with discipline outperform a busy portfolio of undisciplined trades in virtually every long-term study.

The Comparison Trap

In any given period, some asset — whether it is cryptocurrency, a single tech stock, or a sector ETF — will have outperformed your portfolio dramatically. The temptation to measure your results against the best-performing asset of the last six months creates a perpetual cycle of chasing the last winner and abandoning the current strategy.

Every great investor who has compounded capital over decades did so by having a clear strategy and staying the course through periods when that strategy underperformed something else. Consistency and process adherence compound just like money does — slowly at first, then dramatically.

| The Rules-Based Antidote

Having defined entry criteria, position sizing rules, and exit strategies before you invest removes most emotional decisions from the equation. A rules-based approach does not eliminate losses — nothing does. It ensures that your process is repeatable, your mistakes are learnable, and your edge compounds over time rather than eroding. |

Start Right. The Rest Is Practice.

Investing is a learnable skill. It is not reserved for finance professionals or people who understand economic theory. It is available to anyone who builds the right habits from the beginning.

The framework from this guide in plain terms:

- Investing beats saving because compounding at market returns dwarfs savings account rates over time

- There are two paths — passive and active — and the most effective approach uses both

- Start with a broad-market ETF or index fund as your core holding

- Apply position sizing, stop-losses, and risk/reward discipline from your very first position

- Open an account, fund it, and set up automatic contributions — the mechanics are simpler than the anxiety around them

- Build a rules-based process and protect it from the three mindset traps that end most beginners’ journeys

What comes next is building real investing skill — learning to identify setups, manage positions across multiple instruments, and grow both your passive foundation and your active edge simultaneously. That is what ATGL is built to help you do.

| Take the Next Step With ATGL

At AboveTheGreenLine.com we give investors the rules-based system to go from beginner to skilled — covering both passive portfolio construction and active trading strategy. If you’re ready to stop reading and start building, join us Above the Green Line and get access to the full system, real-time trade alerts, step-by-step educational content, and a community of investors who take the process as seriously as you do. |

Frequently Asked Questions

What is the best investment for a beginner?

For most beginners, a low-cost broad-market index fund or ETF — such as a total U.S. market fund or S&P 500 fund — is the best starting point. It provides instant diversification, low fees (0.03–0.05%), and a return that tracks the overall stock market without requiring stock-picking skill or active management. Start here, then expand as your knowledge grows.

How much money do you need to start investing?

Many major brokers now have $0 account minimums, and ETFs can be purchased for the price of a single share. The more important question is how much you can commit consistently over time. Even $50–$100 per month invested automatically in a low-cost index fund compounds meaningfully over a decade. Starting with a small amount is infinitely better than waiting until you have a larger amount.

Is investing in stocks good for beginners?

Yes — with the right approach. Broad-market ETFs and index funds give beginners stock market exposure without requiring individual stock selection. Individual stock picking is higher risk and demands research skill, position sizing discipline, and clear exit rules. Beginners who want to explore individual stocks should start with a small position size and a pre-defined stop-loss before they enter their first position.

What is the difference between saving and investing?

Saving means keeping money in low-risk, accessible accounts (savings accounts, money market funds) where it earns minimal return but is safe. Investing means deploying capital into assets like stocks or ETFs that carry more risk but offer higher potential long-term returns. The key distinction is risk and time horizon — savings is for money you may need within 1–2 years; investing is for capital you can leave working for 3+ years.

Related Articles

[pt_view id=”9b64b383ox”]