By Andrew Stowers

Updated May 3, 2026

The financial industry employs roughly 330,000 investment advisors in the United States. Every one of them has a business reason to tell you that you need professional help.

This guide has a different agenda: giving you the honest analysis of when an investment advisor genuinely earns their fee — and when self-directed investing, done with the right framework, produces a better financial outcome. Both cases are real. The question is which applies to you.

Understanding investment advisors — their types, their fee structures, their regulatory obligations, and the compound mathematics of what their fees actually cost — is the foundation of making that decision correctly. After reading this article, we encourage you to read our Investment Strategy Guide to see how this all fits into the bigger picture.

What Investment Advisors Actually Do — and Don’t Do

| Quick Answer

An investment advisor provides professional guidance on securities selection, portfolio construction, and asset allocation — typically in exchange for an ongoing fee. Registered Investment Advisors (RIAs) are legally registered with the SEC or state regulators. The scope of services varies widely: some manage portfolios only; others provide comprehensive financial planning. |

At the core, an investment advisor’s job is to help clients make better decisions with their money than they would make alone — whether through better asset allocation, more disciplined rebalancing, smarter tax management, or simply providing the guardrails that keep emotionally reactive investors from making costly mistakes.

What Advisors Provide

The primary services of a full-service investment advisor include: asset allocation strategy, investment selection, portfolio rebalancing, tax-loss harvesting, retirement income planning, and — often the most valuable — behavioral coaching that prevents panic-driven decisions during market downturns.

What Advisors Don’t Provide

Investment advisors cannot guarantee returns, eliminate risk, or consistently outperform the market. Research consistently shows that the majority of actively managed funds underperform their benchmark index over periods of 10+ years, net of fees. This is not a criticism of advisors as individuals — it reflects the mathematical challenge of generating consistent alpha in competitive, efficient markets.

Understanding this distinction — between the genuine services an advisor provides and the outcomes that no advisor can reliably deliver — is the starting point for evaluating whether professional advice is worth the cost.

Types of Investment Advisors: Understanding the Landscape

The investment advisory industry is regulated across multiple frameworks with meaningfully different standards. The type of advisor you work with determines their legal obligations to you — and understanding this difference is the single most important factor in advisor selection.

Registered Investment Advisors (RIAs)

RIAs are registered with the SEC (if managing over $110M) or state securities regulators. They are held to a fiduciary standard — legally required to act in the client’s best interest at all times. This is the highest standard of care in the investment advisory profession.

Broker-Dealers

Broker-dealers are registered with FINRA and held to a suitability standard — they must recommend products that are suitable for the client, but not necessarily the best option available. Broker-dealers may earn commissions from the products they sell, creating a structural conflict of interest that the suitability standard does not eliminate.

Certified Financial Planners (CFPs)

CFP is a credential, not a regulatory designation. A CFP may be a fiduciary RIA or a commission-based broker-dealer — the credential alone does not guarantee fiduciary duty. Always ask separately whether the advisor is a fiduciary — the CFP designation does not answer that question.

Robo-Advisors

Automated portfolio management platforms (Betterment, Wealthfront, Vanguard Digital Advisor) use algorithms to manage diversified portfolios at low cost. Most are RIAs and therefore fiduciary. They charge 0.00–0.25% annually — a fraction of traditional advisor fees — but offer limited customization and no human relationship.

| Feature | Fiduciary RIA | Broker-Dealer | Robo-Advisor |

|---|---|---|---|

| Legal Standard | Fiduciary (best interest) | Suitability | Fiduciary (algorithmic) |

| Compensation | Fee-only or fee-based | Often commission-based | % AUM (low) |

| Conflicts of Interest | Low | Higher | Very Low |

| Human Relationship | Yes | Yes | No/limited |

| Typical Cost | 0.5–1.5% AUM | Variable | 0–0.25% AUM |

How Investment Advisors Are Paid: Fee Structures Explained

Fee structure is the second most important evaluative factor after fiduciary status. How an advisor is compensated directly shapes their incentives — and your costs.

| Structure | Typical Cost | Conflict of Interest | Best For |

|---|---|---|---|

| AUM % | 0.5–1.5% annually | Low–moderate | Ongoing management |

| Flat annual retainer | $2,000–$10,000+ | Low | Large portfolios |

| Hourly | $150–$400/hr | Low | Specific questions |

| Commission-based | Varies by product | High | (Favour avoiding) |

| Robo-advisor | 0–0.25% AUM | Very low | Systematic mgmt |

The AUM Percentage Model: Incentives and Limitations

The 1% AUM model is the most common fee structure for traditional advisors. It aligns some incentives — the advisor earns more as your portfolio grows — but creates no accountability for performance. Whether the advisor outperforms, underperforms, or matches the market, the fee is the same. For large portfolios ($1M+), even a lower AUM percentage generates substantial fees that may not be justified by the services received.

Fee-Only vs Fee-Based

Fee-only advisors earn exclusively from client fees — no commissions, no product referrals. This eliminates the most common conflict of interest. Fee-based advisors charge fees but may also earn commissions — the conflict of interest exists but is disclosed. When evaluating advisors, fee-only is structurally preferable; the advisor’s income depends entirely on client satisfaction, not product sales.

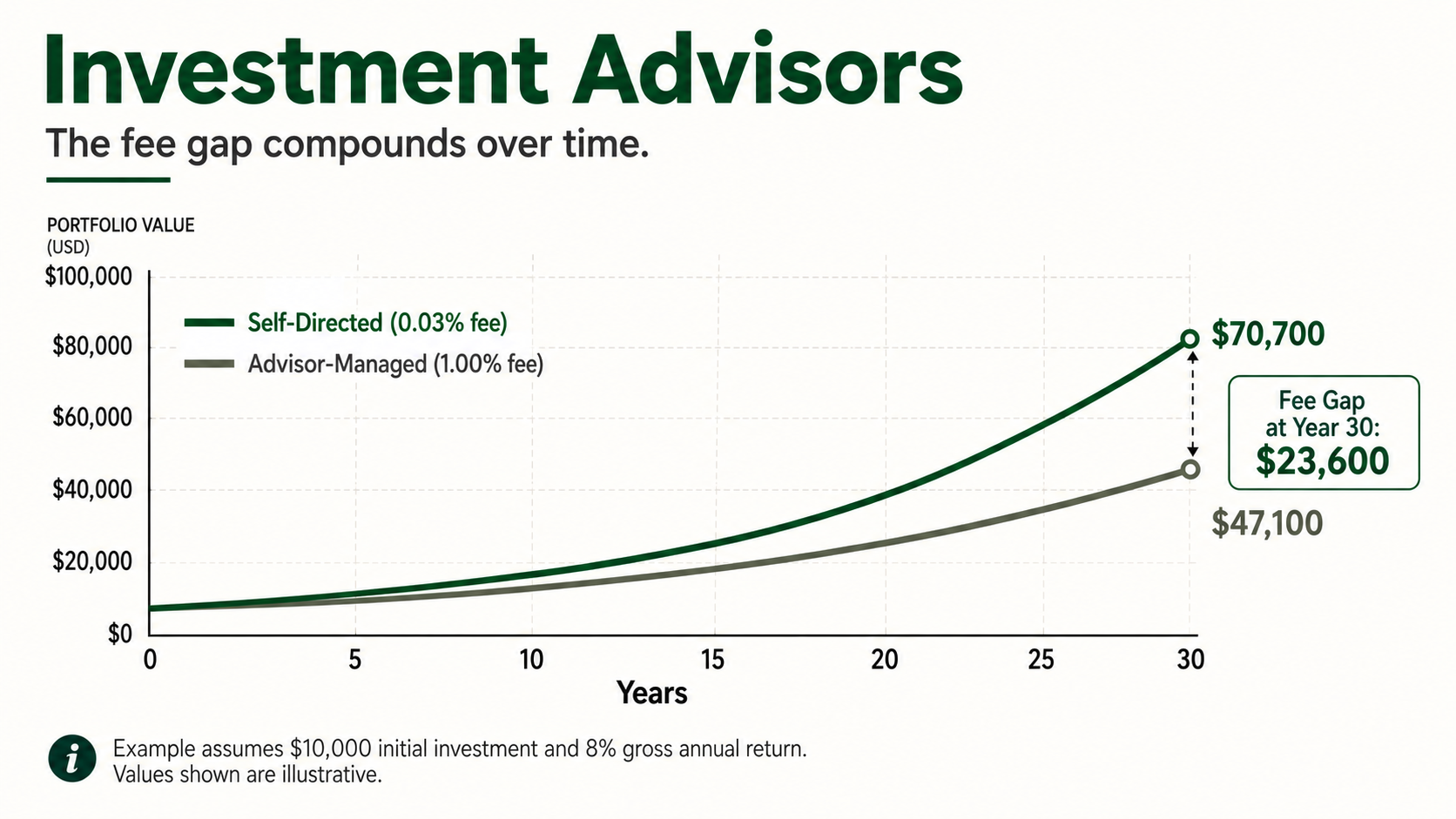

The Hidden Cost of the 1% Fee: What Advisor Fees Actually Cost You

| The Compounding Math

A 1% annual advisory fee on a $500,000 portfolio costs $5,000 in year one. Over 30 years at 7% average market return, the compounding drag of that fee reduces your ending balance by approximately $350,000–$400,000 compared to a 0.03% index fund portfolio. The fee is not 1% per year — it is decades of compounding working against you. |

The compound drag of a 1% annual fee is the most important number most advisor clients never calculate. Here is what it looks like:

| Scenario | 30-Year End Balance | Total Fees Paid | Difference |

|---|---|---|---|

| Self-managed (0.03% ER) | ~$3,817,000 | ~$4,500 | Baseline |

| Robo-advisor (0.25%) | ~$3,570,000 | ~$37,000 | ~$247,000 less |

| Traditional advisor (1.0%) | ~$3,017,000 | ~$152,000 | ~$800,000 less |

Assumes $500,000 initial investment, 7% gross annual return, 30-year horizon. Illustrative calculations — verify with a compound return calculator.

The critical implication: to justify a 1% advisory fee, an advisor must consistently generate approximately 1% per year of alpha above what the investor would earn self-managing a low-cost index portfolio. Research shows that most active managers fail to achieve this consistently over 10+ year periods. The Vanguard Advisor Alpha study estimates advisors can add approximately 1.5% in value annually — but primarily through behavioral coaching and tax management, not investment selection.

This does not mean advisors are never worth hiring. It means the bar for justifying the fee is specific and high — and for many investors with straightforward portfolios, self-direction clears that bar.

When an Investment Advisor Genuinely Adds Value

A balanced analysis requires acknowledging the scenarios where professional advice genuinely earns its cost. There are several — and for investors in these situations, the fee is well justified.

Complex Tax Situations

Roth conversion ladders, tax-loss harvesting at scale, multi-state tax issues, and charitable giving strategies (donor-advised funds, qualified charitable distributions) are areas where professional guidance regularly produces value that exceeds the advisory fee. The complexity here genuinely benefits from professional coordination.

Estate Planning and Wealth Transfer

Trust structures, beneficiary designations, generational wealth strategies, and estate tax mitigation require coordination between investment management, legal planning, and tax strategy. This multi-dimensional complexity is where advisory relationships are most clearly justified.

Concentrated Equity Positions

Executives with large company stock positions, RSU holders, and employees with significant unvested equity face the challenge of diversifying without triggering catastrophic capital gains events. Structured selling, exchange funds, charitable remainder trusts, and collars all require sophisticated strategy that benefits from professional guidance.

Behavioral Coaching

The most consistently documented and arguably most valuable advisor service is preventing clients from making emotionally reactive decisions — panic selling during downturns, overconcentrating in recent winners, abandoning a sound strategy because something else looked better last quarter. Vanguard’s research suggests this behavioural component can add approximately 1.5% in annual value — the strongest single argument for advisory relationships for investors prone to emotional decision-making.

Life Transitions

Receiving an inheritance, selling a business, divorce settlement, or transitioning from wealth accumulation to retirement income distribution — one-time complexity events that benefit from targeted professional guidance even for investors who self-direct the rest of the time.

The Self-Directed Alternative: When You Don’t Need an Advisor

| The Profile

Self-directed investing produces better net outcomes for investors who: have a straightforward portfolio (primarily stocks and ETFs), are willing to invest time in financial education, have no extreme complexity (no concentrated positions, no complex estate needs), and can manage their own emotional reactions to market volatility. The compounding savings on advisory fees are the single largest financial advantage of self-direction. |

For the right investor — and this describes a large proportion of self-directed individuals — the case for avoiding traditional advisor fees is compelling purely on the mathematics.

The Self-Directed Toolkit

A disciplined self-directed investor needs four things: a broad-market index ETF allocation as the core (capturing market returns at near-zero cost), a rules-based active strategy as the satellite (for those who want to participate actively), a rebalancing discipline (annually or at defined drift thresholds), and the emotional framework to execute the plan during market stress rather than improvising.

Where Self-Direction Has Real Limits

Tax optimisation at scale, estate planning, complex equity compensation, and major life transitions are areas where targeted professional engagement is often still worth the cost — even for investors who otherwise self-direct. The key distinction: targeted hourly or project-based advice for specific complexity versus an ongoing 1% AUM relationship for a straightforward portfolio.

The ATGL approach: providing the rules-based framework, strategy education, and investment community that gives self-directed investors the structure, discipline, and ongoing learning that advisors provide — without the compounding 1% annual fee.

How to Evaluate and Choose an Investment Advisor

For investors who determine professional advice is right for their situation, due diligence is non-negotiable. The advisory relationship involves significant trust and significant fees — it deserves the same rigour you would apply to any major financial decision.

Step 1: Verify Registration and Regulatory History

Search the SEC’s Investment Adviser Public Disclosure database at adviserinfo.sec.gov. This free resource shows any advisor’s registration status, regulatory history, disciplinary actions, and whether any complaints have been filed. Run this search before any substantive conversation.

Step 2: Confirm Fiduciary Status in Writing

Ask directly: ‘Are you a fiduciary at all times, on all services you provide to me?’ Some advisors are fiduciary for investment management but not for insurance or annuity recommendations. Fiduciary status should be confirmed in writing in the advisory agreement — verbal assurances are not sufficient.

Step 3: Understand Total Cost

The advisor’s fee is not the only cost. Add: expense ratios of any funds recommended (proprietary funds often carry higher ERs), transaction costs, and any platform fees. Total cost of ownership may be meaningfully higher than the headline advisory fee.

Key Questions to Ask Any Advisor

- Are you a fiduciary at all times on all services — and will you confirm this in writing?

- How are you compensated — and do you receive any commissions, referral fees, or other third-party payments?

- What is your investment philosophy — and what benchmark do you use to measure performance?

- What has been your average client’s net return versus the relevant benchmark over the past 5 and 10 years?

- How many clients do you serve — and what is your typical client-to-advisor ratio?

- Do you have any regulatory disclosures, complaints, or disciplinary actions on your record?

- What is your process for communicating with clients during market downturns?

Red Flags

- Reluctance to confirm fiduciary status in writing

- Recommendation of proprietary or high-fee funds without clear justification

- Any language suggesting guaranteed or ‘market-beating’ returns

- Pressure to decide quickly or invest before conducting due diligence

- Inability or unwillingness to explain fee structure in plain English

The Bottom Line on Investment Advisors

Investment advisors provide genuine value in specific situations — and for investors in those situations, the fee is a sound investment. Complex tax optimization, estate planning, concentrated equity positions, and behavioral coaching are all areas where professional expertise consistently pays for itself.

For investors with straightforward portfolios, the mathematical case runs the other way. The compounding drag of a 1% annual fee on a long-term portfolio is the financial equivalent of a second mortgage on your retirement — and for investors willing to develop their own rules-based approach, self-direction is the better financial outcome.

The decision is not ‘advisors are good’ or ‘advisors are bad’ — it is whether your specific situation clears the bar for professional advice to add more value than the fee extracts.

| Build Your Own Rules-Based System With ATGL

At AboveTheGreenLine.com we provide the framework, education, and investment community that gives self-directed investors the structure and discipline of a professional system — without the ongoing 1% advisory fee. If you’re ready to take control of your own investing journey, join us Above the Green Line. |

Frequently Asked Questions

What is the difference between a financial advisor and an investment advisor?

An investment advisor specifically provides advice on securities and portfolio management. A financial advisor is a broader term covering professionals who advise on overall financial planning — budgeting, insurance, tax planning, and estate planning in addition to investments. All investment advisors are financial advisors in a general sense, but not all financial advisors focus specifically on securities and portfolio construction.

How much does it cost to have an investment advisor?

Traditional investment advisors typically charge 1% of assets under management annually — meaning a $500,000 portfolio costs $5,000 per year. Fee-only advisors may charge flat annual retainers ($2,000–$10,000+) or hourly rates ($150–$400). Robo-advisors charge 0.25% or less. Commission-based advisors earn from product sales. The total cost of ownership — including fund expense ratios — is often higher than the headline advisory fee.

Is it worth paying for an investment advisor?

It depends on your situation. Advisors add genuine value for investors with complex tax situations, estate planning needs, concentrated equity positions, or those prone to emotional market decisions. For investors with straightforward portfolios who are willing to self-direct using a rules-based approach, the compounding drag of a 1% fee — potentially $350,000–$400,000 over 30 years on a $500,000 portfolio — often makes self-direction the better financial outcome.

How do I find a fiduciary investment advisor?

Search the SEC’s Investment Adviser Public Disclosure database at adviserinfo.sec.gov to verify any advisor’s registration and regulatory history. The NAPFA (National Association of Personal Financial Advisors) directory lists fee-only fiduciary advisors. Always ask directly and in writing: ‘Are you a fiduciary at all times, on all services?’ — not just for investment management.

Related Articles

[pt_view id=”9b64b383ox”]