By ATGL

Updated November 9, 2024

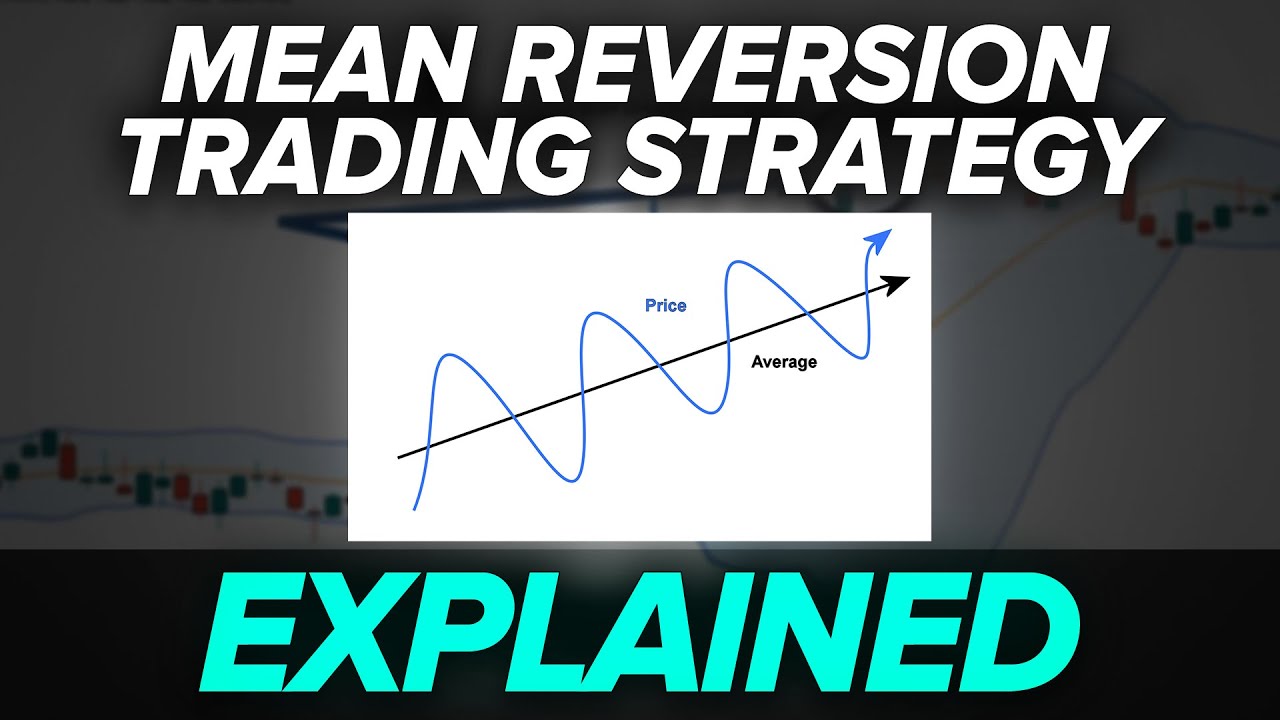

Investors often grapple with market unpredictability, continually seeking strategies to gain an edge. One such intriguing concept is mean reversion, an idea that encourages looking for patterns and returns to average values over time. Understanding mean reversion can unveil essential insights into market behavior and enhance investment strategies.

At its core, mean reversion posits that asset prices fluctuate around a historical average, making it a critical concept in both theoretical finance and practical trading. Grounded in theories like the Efficient Market Hypothesis and reinforced by statistical principles, mean reversion offers investors a structured way to approach price analysis. By exploring market dynamics and psychological factors, traders can identify opportunities bound to revert to their mean.

In this article, we will thoroughly dissect mean reversion, delving into its calculation methods, integration with technical analysis, and its multifaceted applications in trading strategies. We will also discuss the benefits and limitations of this approach, supported by real-world examples, ultimately equipping investors with the knowledge to navigate their portfolios with greater confidence.

What is Mean Reversion?

Mean reversion is a financial theory positing that asset prices and returns tend to gravitate back toward their historical average over time. This theory helps identify market anomalies and inefficiencies, suggesting that extreme price movements are temporary and will eventually stabilize.

Traders use mean reversion strategies by buying undervalued assets and selling overvalued ones, betting on price normalization. Key indicators like Bollinger Bands and moving averages help determine entry and exit points based on this principle. However, market conditions can impact these strategies, as prolonged trends might prevent the expected return to the mean.

Reversion trading strategies are popular in volatile and range-bound markets where frequent price fluctuations offer buying and selling opportunities. Understanding market dynamics through statistical analysis of historical returns and standard deviation can enhance the effectiveness of reversion strategies. Despite its appeal, the success of mean reversion depends on accurately recognizing when an asset has reached extreme conditions and predicting its movement back to the long-term mean.

Theoretical Foundation of Mean Reversion

Mean reversion is a financial theory suggesting that asset prices and historical returns gravitate towards their long-term average levels. This theory views extreme price movements as outliers, indicating that such deviations are not sustainable over time. The greater a price deviates from the historical mean, the higher the likelihood it will realign with the average.

Mean reversion is versatile, applying across various asset classes such as stocks, bonds, and commodities. The fundamental premise is that extreme values are temporary, and financial metrics will eventually revert to typical levels given sufficient time.

Efficient Market Hypothesis

The Efficient Market Hypothesis (EMH) posits that financial markets efficiently incorporate all available information, continuously reflecting it in asset prices. As a key component of modern financial theory, the EMH suggests the complexity of identifying undervalued stocks and predicting future performance.

The EMH is often challenged by mean reversion theory, which argues that markets can either overreact or underreact to new information, creating temporary price distortions. These distortions are believed to correct over time, questioning the absolute efficiency suggested by the EMH.

Statistical Concepts

Mean reversion can be assessed through statistical analysis, focusing on how much an asset price deviates from its historical mean. Standard deviation is a crucial tool in this analysis, quantifying the volatility around the mean and providing insights into typical price deviations.

A systematic mean reversion trading approach involves identifying overbought or oversold conditions based on deviations from the historical average. Traders utilize statistical thresholds, defined by the number of standard deviations, to recognize potential mean reversion opportunities in the market.

Mechanisms of Mean Reversion

Mean reversion is a financial theory suggesting that asset prices and historical returns tend to revert to their long-term mean or average level. This phenomenon is often driven by economic indicators and historical price performance. The greater the deviation from the mean, the higher the probability that the next price movement will be closer to this average, reflecting a natural oscillation back toward typical levels after experiencing extreme fluctuations.

Technical analysis tools like moving averages, Bollinger Bands, and oscillators such as the Relative Strength Index (RSI) are frequently employed to identify mean reversion opportunities. These tools help traders spot overbought or oversold conditions, providing signals based on statistical analysis for potential reversion situations. The Vasicek model exemplifies mean reversion by describing how interest rates, when deviating from average levels, are drawn back towards a long-term mean.

While mean reversion is a sound concept, it has limitations. It assumes that prices will return to normal, which is not guaranteed. Some significant price changes may indicate a new normal for the asset, making reversion strategies less effective.

Price Fluctuations and Market Dynamics

Mean reversion posits that asset prices and market returns eventually gravitate toward their historical averages. Extreme price fluctuations are typically temporary, indicating a predictable pattern within market dynamics. This provides arbitrage opportunities when prices deviate from their means due to irrational behavior or delayed reactions to new information, helping investors navigate market fluctuations.

The cyclic nature of mean reversion is evident as greater deviations from the mean increase the probability of asset prices returning closer to that mean. Understanding this cycle allows investors to develop informed investment strategies based on anticipated price movements, taking advantage of the predictable nature of market dynamics.

Market Psychology and Behavior

Investors frequently overreact to current events and information, leading to speculative valuations and increased market volatility. This risk aversion often results in investors holding onto equities after negative news, with equity prices gradually returning to profitability as negative sentiment fades. The attraction of lower equity prices motivates investors to buy, seeking future profits and influencing market dynamics.

Mean reversion suggests that such market anomalies often correct themselves over time. Excessive reactions to news or financial reports result in temporary mispricings that tend to revert. This behavior is also influenced by the availability bias, with investors making decisions based on readily available information rather than thorough analysis.

Calculation Methods

Mean reversion is a financial theory that emphasizes the tendency of asset prices to return to their historical average over time. This theory utilizes statistical measures and calculations to identify potential reversion opportunities. Various methods including regression analysis, time series analysis, and hypothesis testing help demonstrate mean reversion in asset prices effectively. These strategies focus on detecting significant deviations from the mean, which can trigger trading signals for potential buying or selling.

Moving Averages

Moving averages play a crucial role in smoothing price data to highlight trends, making them essential for identifying mean reversion opportunities. The two most common types include the Simple Moving Average (SMA), which averages closing prices over a specified period, and the Exponential Moving Average (EMA), which gives more weight to recent prices. Traders often combine these averages with other technical indicators to better identify mean prices and make informed trading decisions, especially in range-bound markets.

Z-Scores

Z-Scores are valuable in measuring how many standard deviations a current price deviates from the mean price, aiding in the identification of extreme price movements. The formula Z-Score = (Current Price – Mean Price) / Standard Deviation provides insights into the asset’s valuation relative to its average. Z-Scores help traders spot overbought or oversold conditions by using thresholds such as ±1.5 or ±2. High Z-Scores, indicating extreme conditions, can signal potential reversion points in volatile markets.

Integration with Technical Analysis

Mean reversion strategies leverage technical analysis to identify potential trading opportunities based on asset prices deviating from historical averages. Tools like moving averages and statistical measures help traders gauge the extent of price deviations. By analyzing these deviations, traders aim to develop strategies predicting that prices will revert to their long-term mean over time.

However, market conditions, such as economic events, can disrupt mean-reverting patterns. It’s crucial for traders to integrate mean reversion with other technical analysis techniques like moving average crossovers to anticipate temporary and predictable price movements.

Bollinger Bands

Bollinger Bands are a popular tool in mean reversion strategies, consisting of a moving average with two standard deviation lines plotted above and below. These bands expand and contract in response to market volatility. When an asset’s price moves outside the bands, it is often seen as overbought or oversold, signaling potential mean reversion opportunities.

Traders leverage Bollinger Bands to determine entry and exit points by observing how prices behave in relation to these bands. Typically calculated using a 20-day simple moving average, Bollinger Bands offer insights into whether an asset is trading at an extreme compared to its recent price performance.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a momentum oscillator that evaluates speed and change in price movements, ranging from 0 to 100. An RSI value above 70 suggests the asset might be overbought, while a value below 30 implies it might be oversold, indicating potential mean reversion points.

Traders utilize the RSI to recognize when an asset’s price might revert to its historical average. Particularly in volatile markets, the RSI serves as a risk management tool, helping traders set stop-loss orders around the mean and identify take-profit points for assets above their historical averages.

Trading Strategies Based on Mean Reversion

Mean reversion is a financial theory that asserts asset prices will revert to their historical average over time. Traders use this concept to identify price deviations from the mean to profit from corrective movements. Technical indicators such as Bollinger Bands, RSI, Stochastic Oscillator, and MACD are commonly employed to recognize overbought or oversold conditions. These tools help traders set clear entry and exit points, enhancing their strategies across various asset classes.

Day Trading Strategies

In day trading, mean reversion strategies involve buying and selling assets within a single day. Traders rely on indicators like RSI, Stochastic Oscillator, and Bollinger Bands to spot market extremes. Well-defined entry and exit points are crucial to capitalize on short-term price fluctuations. Effective risk management is achieved through stop-loss orders, which are placed just outside identified overbought or oversold levels to safeguard positions.

Swing Trading Techniques

Swing traders utilize mean reversion strategies to capture small, intraday profits as prices revert to their historical averages. This approach is versatile, applicable to stocks, forex, commodities, and indices. Technical indicators such as RSI and Bollinger Bands are instrumental in identifying trading opportunities. Clear entry and exit points help in setting stop-loss orders, mitigating risk as prices overreact to news and events.

Long-Term Investment Applications

Long-term investors often adopt strategies aligned with mean reversion, capitalizing on price corrections back to historical averages. Markets with slower reversion rates, like K.O.S.P.I., offer stability for long-term investment. Mean reversion helps investors understand and predict the rate at which asset prices revert, fostering effective long-term strategies. By focusing on historical price patterns, investors can better navigate market volatility and manage risk through informed decision-making.

Benefits of Mean Reversion

Mean reversion offers traders a clear framework for making trading decisions by providing identifiable entry and exit points. This is achieved through strategies like stop-loss orders around the mean price, limiting investment risk. As a short-term trading strategy, it exploits intraday price movements, thus presenting numerous opportunities for profit.

Mean reversion indicators effectively identify overbought and oversold conditions, aiding traders in the decision-making process. The strategy supports the belief that significant deviations from historical averages can result in lucrative opportunities, reinforcing the potential for compounding earnings. Furthermore, it contributes to the accurate pricing of options by relying on historical average prices, assisting traders in making informed decisions on call or put contracts.

Predictability and Planning

According to the mean reversion theory, extreme price points in equity markets are often followed by a return to long-term averages. This presents a foundation for predicting future price movements. In volatile markets, mean reversion can help investors pinpoint buying opportunities in significantly undervalued assets, anticipating a rebound towards historical averages.

The concept provides room to capitalize on temporary market distortions, as prices frequently revert to their means. However, it’s essential to note that economic events can disrupt these mean-reverting patterns, implying that while predictability is often present, external factors can influence actual price behavior. Moreover, mean reversion challenges notions of market efficiency by revealing potential arbitrage opportunities.

Risk Management Implications

Understanding mean reversion is crucial for risk management, allowing traders to hedge potential losses when stock prices deviate from historical averages. Recognizing overbought or oversold conditions with this approach helps avoid entering or maintaining positions at unsustainable levels, enhancing overall risk management strategies.

By identifying extreme price movements through mean reversion techniques, traders can set effective stop-loss orders, limiting potential losses. These strategies exploit market inefficiencies, giving traders a method to capitalize on temporary mispricings while adequately managing associated risks. For successful execution, assessing the risk and potential reward of selected securities is crucial, driving effective decision-making in risk management contexts.

Limitations of Mean Reversion

Mean reversion is a financial theory predicting that asset prices will eventually return to their historical average. However, this strategy can struggle in markets with strong trends, where prices deviate from their mean over extended periods. Timing these reversion patterns is risky, as economic news or events can disrupt this mean-reverting behavior, leading to possible losses.

Market Exceptions

Market anomalies and unforeseen events, like Black Swan events, can prevent prices from reverting to their historical average, undermining the assumptions of mean reversion. Additionally, market manipulation and insider trading can distort typical price movements, making mean reversion strategies unreliable. The efficient market hypothesis may oversimplify dynamics, further challenging the effectiveness of this strategy as a predictive tool.

Timing and Volatility Challenges

Implementing mean reversion strategies demands precise timing and patience, as anticipated reversion can take longer to materialize, especially in volatile conditions. While volatility can support mean reversion strategies, excessive market fluctuations can impede their success. Additionally, when high-frequency trading accompanies mean reversion, significant transaction costs might arise, posing further challenges to profitability.

Real-World Applications

Mean reversion strategies are versatile tools in trading and can be applied to stock prices, volatility, earnings, and market performance. Traders leverage historical data to identify an asset’s average price, using this information to spot significant deviations and make informed trading decisions. This approach is particularly useful for risk management by signaling overbought or oversold conditions. Algorithmic trading algorithms frequently employ mean reversion techniques to find buying and selling opportunities, using technical indicators such as moving averages and RSI to pinpoint extreme price deviations and optimize trade timing.

Case Studies of Mean Reversion in Financial Markets

The dot-com bubble of the late 1990s exemplifies mean reversion, where inflated technology stocks corrected over time. Similarly, during the 2008 financial crisis, commodity prices that plummeted eventually reverted to mean levels. In bond markets, mean reversion guides central banks’ interest rate adjustments to maintain rates near target means, affecting bond prices and yields. Stock prices often demonstrate mean reversion, as prices above historical averages may indicate overvaluation and the likelihood of a correction.

Portfolio Management Strategies

Mean reversion strategies significantly influence diversification and rebalancing in portfolio management. Investors may rebalance portfolios during downturns, forecasting asset prices to revert to historical averages. This strategy can also help investors identify underpriced assets, presenting opportunities for gains when prices recover. By incorporating mean reversion concepts, portfolio management fosters disciplined investing aligned with historical price patterns, aiding in managing volatility and reducing emotional responses to market changes.

Join Above the Green Line today and learn how about our banana hunt trading strategy and how it mirrors the reversion to the mean.

Related Articles

[pt_view id=”9b64b383ox”]