By Andrew Stowers

Updated May 23, 2026

Corporate bonds occupy a specific and useful position in the investment universe — offering more income than government bonds while carrying less risk than equities, at least for investment grade issuers.

But the term ‘corporate bonds’ covers an enormous spectrum: from AAA-rated blue-chip debt that trades within a few basis points of Treasury yields, to distressed high yield paper that behaves more like equity than fixed income during a market downturn. Understanding where on that spectrum you are positioned — and what drives the risk and return characteristics at each point — is the foundation of using corporate bonds intelligently. If you want to learn more about ETFs in general after finishing this article, we highly encourage all of our readers to look over our ETF Investing Guide.

What Are Corporate Bonds and How Do They Work?

| Quick Answer

Corporate bonds are debt securities issued by companies to raise capital — the company borrows money from investors and promises to pay a fixed interest rate (coupon) over a defined period, then return the principal at maturity. They offer higher yields than government bonds to compensate for credit risk, with actual yield depending heavily on the issuer’s financial strength. |

When a company needs to raise capital, it has two primary options: sell equity (shares) or issue debt (bonds). Corporate bonds represent the debt route. The company borrows from investors under defined terms — a fixed interest rate, a maturity date, and a promise to return the full principal — and investors receive regular income in exchange for lending their capital.

How Corporate Bonds Work: The Four-Step Mechanics

- Company issues bonds at face value (typically $1,000 per bond) with a stated coupon rate and maturity date

- Investors buy bonds at issuance in the primary market, or subsequently in the secondary over-the-counter (OTC) market

- The company pays the coupon interest semi-annually throughout the bond’s life — a 5% coupon on a $1,000 bond pays $25 every six months

- At maturity, the company returns the full face value to bondholders — $1,000 per bond regardless of the price paid in the secondary market

Key Structural Terms

Face value (par): the amount returned at maturity — typically $1,000; the reference value for coupon calculations.

Coupon rate: the fixed annual interest payment as a percentage of face value; does not change after issuance; set at a level that reflects market rates and the issuer’s credit quality at the time of issuance.

Maturity: when the bond expires and principal is repaid; ranges from short (1-3 years) to medium (3-10 years) to long (10-30+ years); longer maturities carry more interest rate risk.

Why Companies Issue Bonds — and Why Investors Buy Them

For companies: bond financing is often cheaper than equity financing — interest payments are tax-deductible, and issuing bonds does not dilute existing shareholders. For investors: corporate bonds provide predictable, contractual income above what government bonds offer, with a defined return of principal if held to maturity.

A critical structural protection: in the event of corporate bankruptcy, bondholders are paid before equity shareholders. Corporate bonds rank above common stock in the capital structure — this priority claim provides meaningful downside protection relative to owning equity in the same company.

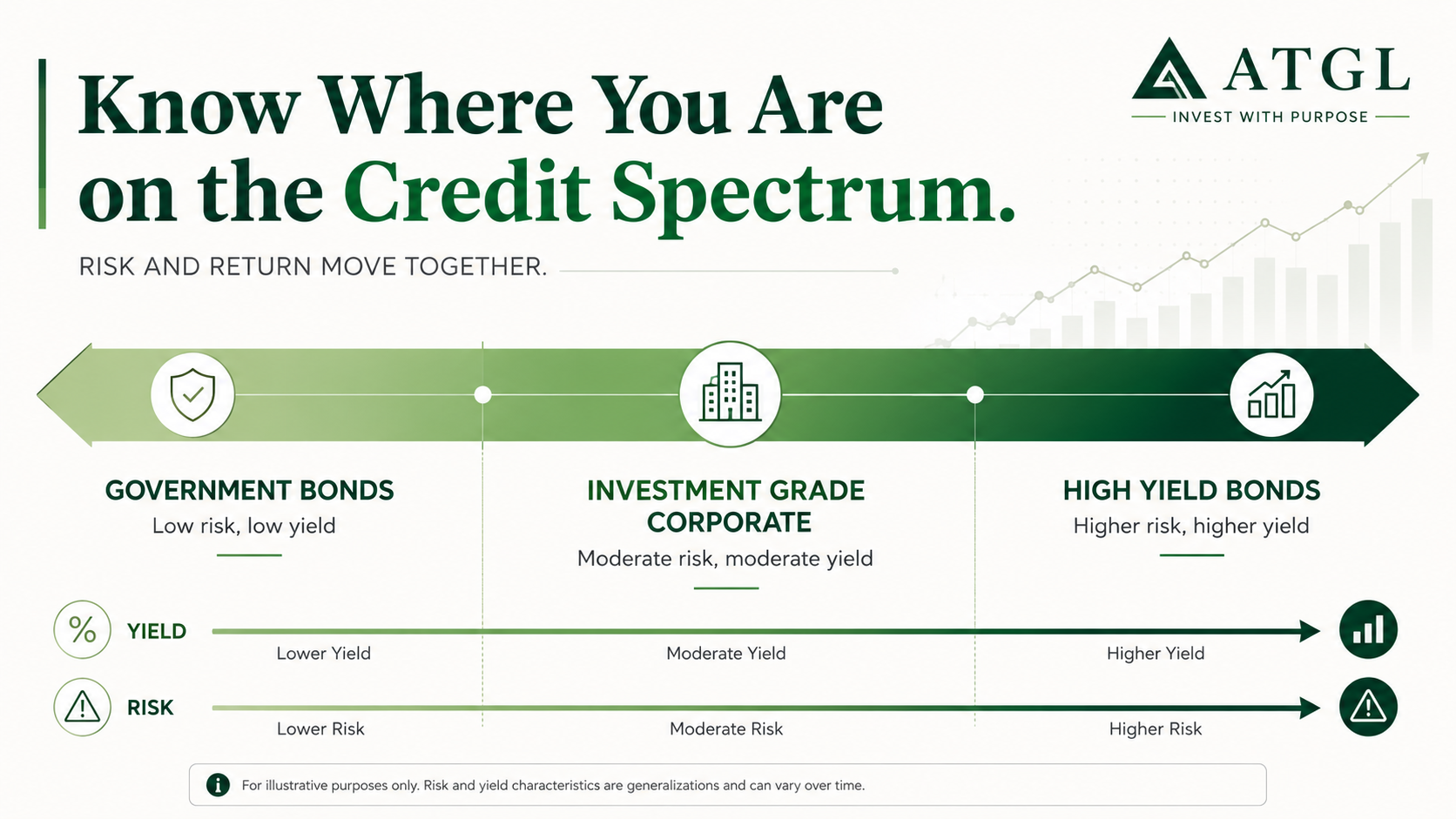

Investment Grade vs High Yield: The Most Important Credit Distinction

| The Core Classification

Corporate bonds divide into two broad categories: investment grade (rated BBB-/Baa3 or above) — lower default risk, lower yield — and high yield, also called junk bonds (rated below investment grade) — higher default risk, higher yield to compensate. This is the single most important classification for evaluating any corporate bond position. |

Three credit rating agencies — Moody’s, S&P Global, and Fitch — independently assess the creditworthiness of corporate bond issuers. Their ratings express the probability of default: the higher the rating, the lower the assessed likelihood the issuer fails to meet its debt obligations.

| Moody’s | S&P / Fitch | Category | Default Risk |

|---|---|---|---|

| Aaa | AAA | Investment Grade | Highest quality, near-zero |

| Aa1, Aa2, Aa3 | AA+, AA, AA- | Investment Grade | Very high quality |

| A1, A2, A3 | A+, A, A- | Investment Grade | High quality |

| Baa1, Baa2, Baa3 | BBB+, BBB, BBB- | Investment Grade (Lowest) | Adequate capacity to repay |

| Ba1, Ba2, Ba3 | BB+, BB, BB- | High Yield | Speculative elements |

| B1, B2, B3 | B+, B, B- | High Yield | Speculative |

| Caa1–Caa3 | CCC+–CCC- | High Yield | Poor standing, high risk |

| Ca, C | CC, C | High Yield | Near or in default |

| — | D | Default | Default has occurred |

Investment Grade: The Institutional Standard

Investment grade bonds — rated Baa3/BBB- and above — are the foundation of most institutional fixed income portfolios. Pension funds, insurance companies, and sovereign wealth funds are typically restricted by mandate or regulation to investment grade holdings. This institutional demand creates deep liquidity and narrows credit spreads for IG bonds.

Historical average annual default rate for investment grade bonds: approximately 0.1% — representing very low but not zero credit risk. Even the lowest investment grade tier (BBB-/Baa3) has a substantially higher probability of repayment than the public might assume from the ‘near-junk’ perception.

High Yield: Income With Equity-Like Risk

High yield bonds — rated Ba1/BB+ and below — offer meaningfully higher income to compensate for higher default probability. Historical average annual default rates for high yield bonds run approximately 3-5% in normal market environments and spike to 10%+ during recessions.

The critical characterisation for portfolio construction: high yield bonds are NOT defensive assets during equity bear markets. When credit conditions deteriorate and investors flee to safety, high yield spreads widen sharply and bond prices fall — often in close correlation with equity declines. High yield provides income premium but does not provide the portfolio cushion that investment grade bonds offer during equity market stress.

The Fallen Angel

A fallen angel is an investment grade bond downgraded to high yield status. These downgrades force institutional investors who cannot hold sub-investment-grade paper to sell, creating price dislocations that can generate attractive entry opportunities for investors without such constraints. Fallen angels are actively tracked as tactical opportunities by active fixed income managers.

Key Metrics: The Four Numbers Every Corporate Bond Investor Must Know

Understanding corporate bonds as investments requires fluency with four specific metrics. Each tells you something essential about a bond’s return profile and risk level that the others do not.

1. Coupon Rate

The coupon rate is the fixed annual interest payment expressed as a percentage of face value. A $1,000 bond with a 5% coupon pays $50 per year ($25 semi-annually), regardless of what happens to the bond’s market price. The coupon rate is set at issuance and never changes — it reflects market rates and the issuer’s credit quality at the time of issue.

The coupon rate is not the same as the yield — if you buy a bond at a premium (above $1,000) or discount (below $1,000) in the secondary market, your actual yield differs from the stated coupon. This distinction is where yield to maturity becomes essential.

2. Yield to Maturity (YTM)

Yield to maturity is the annualised total return you would receive if you bought the bond at its current market price and held it to maturity, receiving all coupon payments along the way. YTM accounts for any premium or discount to face value paid at purchase — making it the most accurate single measure of a bond’s true return.

The inverse relationship: when market interest rates rise, existing bonds become less attractive (their fixed coupons are now lower than new issuance), so their prices fall and their YTM rises. When rates fall, existing bonds become more attractive, prices rise, and YTM falls. Price and yield always move in opposite directions.

3. Duration

Duration measures how sensitive a bond’s price is to interest rate changes. A bond with a duration of 7 years will move approximately 7% in price for every 1% change in interest rates. Duration is determined primarily by maturity (longer maturity = higher duration) and coupon rate (higher coupon = lower duration, because more cash flows arrive sooner).

Duration is the most important risk metric for corporate bond investors. A portfolio of 10-year investment grade corporate bonds with duration of 8 years will lose approximately 8% in market value if rates rise 1% — even if no defaults occur. Understanding duration before entering any bond position is non-negotiable.

4. Credit Spread

The credit spread is the additional yield a corporate bond offers above an equivalent-maturity U.S. Treasury bond — the market’s compensation for taking on the issuer’s credit risk. Investment grade bonds typically offer spreads of 0.5-2.0% above Treasuries. High yield bonds typically offer spreads of 3-6% above Treasuries in normal markets, widening to 8-15% or more during periods of credit stress.

Credit spread movement is an early warning signal for credit conditions. When spreads are widening — investors demanding more compensation per unit of credit risk — it indicates deteriorating credit conditions or rising recession risk. Narrowing spreads signal improving credit health. Active investors monitor spread levels and direction as a measure of the market’s assessment of credit risk.

Corporate Bonds vs Government Bonds vs Stocks: An Honest Comparison

Corporate bonds occupy the middle of the risk/return spectrum — more income than Treasuries, more stability than equities. But the comparison is more nuanced than a simple middle-ground position suggests.

| Feature | Gov’t Bonds | IG Corporate | HY Corporate | Equities |

|---|---|---|---|---|

| Credit Risk | Near-zero | Low | Moderate–High | N/A (equity) |

| Interest Rate Risk | High | Moderate–High | Moderate | Low (indirect) |

| Typical Yield | Lowest | Low–Moderate | Moderate–High | Variable |

| Recession Behaviour | Strong outperform | Moderate outperform | Underperform | Underperform |

| Correlation to Stocks | Low / negative | Low | High (in stress) | — |

| Best For | Capital preservation | Income + stability | Higher income | Long-term growth |

The 60/40 Portfolio Framework

In the traditional 60% equity / 40% bond portfolio construction, investment grade corporate bonds serve as the income-generating complement to equity volatility. They provide more yield than Treasuries while maintaining a low-to-negative correlation with equities during most market environments — cushioning portfolio declines when stocks fall.

The important caveat: this cushioning effect is specific to investment grade bonds. High yield bonds are highly correlated with equities during stress events — owning 40% high yield provides far less portfolio stability than 40% investment grade. The credit quality of the bond allocation determines whether the diversification benefit is real or illusory.

The Risks Every Corporate Bond Investor Must Understand

Corporate bonds offer more income than government bonds for a reason — they carry risks that government bonds do not. Understanding these four risk categories is essential before any corporate bond investment.

1. Credit Risk (Default Risk)

Credit risk is the possibility the issuer fails to meet coupon payments or repay principal at maturity. Investment grade bonds have historically defaulted at approximately 0.1% annually — very low but not zero. High yield bonds default at approximately 3-5% in normal markets and 10%+ during recessions. Diversification across issuers, sectors, and maturities reduces but does not eliminate credit risk for any individual bond.

2. Interest Rate Risk

As market interest rates rise, existing bond prices fall — proportionally to their duration. A 10-year investment grade corporate bond with 8-year duration loses approximately 8% of its market value for every 1% rise in rates, even if the issuer is entirely sound. This is the primary risk for investors who may need to sell before maturity. Investors holding bonds to maturity receive par value regardless of interim price movements — but must accept below-market income if they locked in a low coupon rate.

3. Call Risk

Many corporate bonds include call provisions allowing the issuer to redeem (call) the bond before maturity at a predetermined call price — typically when market interest rates fall and the company can refinance its debt at a lower rate. This is advantageous to the issuer and disadvantageous to the investor, who loses a high-coupon bond precisely when reinvestment rates are lowest. Called bonds force reinvestment at less attractive rates, reducing total return below initial expectations.

4. Liquidity Risk

Unlike equities and Treasury bonds — which trade on exchanges or in deep electronic markets — individual corporate bonds trade in the over-the-counter (OTC) dealer market. This market has significantly wider bid-ask spreads and less price transparency than exchange-traded markets. Selling a specific corporate bond quickly and at a fair price can be difficult, particularly for bonds from less-known issuers or during periods of market stress. Corporate bond ETFs eliminate this liquidity risk by providing exchange-traded access to the asset class.

How to Invest in Corporate Bonds: Direct Holdings vs Corporate Bond ETFs

| Data Note

All ETF expense ratios are approximate and require verification at fund provider websites before investing. |

Individual investors can access corporate bonds through two main routes, each with distinct advantages and trade-offs.

Route 1: Buying Individual Corporate Bonds Directly

Individual bonds are available through most full-service and online brokerages, either at new issuance (primary market) or through the secondary OTC market. Practical considerations:

- Minimum investment: face value is typically $1,000, but practical secondary market trading requires $5,000-$10,000 per bond for reasonable bid-ask spreads

- Credit analysis required: each issuer must be evaluated individually for default risk — either through personal analysis, rating agency assessments, or with an advisor

- Hold-to-maturity certainty: buying individual bonds and holding to maturity provides exactly the coupon income and par value return specified at purchase — no price risk if not selling before maturity

- Illiquidity: selling before maturity in the OTC market may produce prices meaningfully below fair value

Direct bond ownership is most appropriate for investors with $50,000+ to allocate to corporate bonds who want a defined, predictable income stream and certainty of par repayment — and who are either comfortable conducting credit analysis or working with a fixed income specialist.

Route 2: Corporate Bond ETFs

For most individual investors, corporate bond ETFs provide the most practical access to the asset class: diversification across hundreds or thousands of bonds, full exchange liquidity, no credit analysis burden, and accessible minimum investment (a single ETF share).

| ETF Name | Ticker | Category | Approx. ER | Key Characteristic |

|---|---|---|---|---|

| iShares Investment Grade Corp Bond | LQD | IG Corporate (~10yr duration) | ~0.14% | Core IG exposure |

| iShares High Yield Corporate Bond | HYG | High Yield Corporate | ~0.48% | Most liquid HY ETF |

| SPDR Bloomberg High Yield Bond | JNK | High Yield Corporate | ~0.40% | Broad HY alternative |

| iShares 1-5 Yr IG Corp Bond | IGSB | Short-Duration IG | ~0.04% | Reduced rate risk |

| Vanguard Interm-Term Corp Bond | VCIT | IG Corporate (~7yr duration) | ~0.04% | Low-cost IG option |

Verify all expense ratios at fund provider websites — these change. Tickers and fund names are illustrative.

The Critical ETF Trade-Off: NAV Fluctuation

Corporate bond ETFs do NOT hold bonds to maturity — they continuously roll their holdings to maintain their stated duration. This means ETF investors take full interest rate risk through NAV price changes, unlike a direct bond held to maturity which returns par value regardless of rate movements. An investor in LQD (approximately 8-9 year duration) will see approximately 8-9% NAV decline for every 1% rise in rates — even if no underlying bonds default.

This distinction — direct bond held to maturity vs ETF with floating NAV — is the most important structural difference between the two investment routes and determines which is more appropriate for a given investor’s time horizon and rate sensitivity.

How Corporate Bonds Fit in a Complete Portfolio

Corporate bonds serve meaningfully different roles depending on credit quality and investor profile.

Income-Focused Investor

Investment grade corporate bonds — through LQD, VCIT, or individual bonds — provide reliable semi-annual income above Treasury yields with low default risk. For investors building a fixed income allocation for retirement income or portfolio stability, IG corporate bonds improve the income contribution relative to pure Treasuries without introducing equity-like volatility.

Portfolio Diversification and 60/40 Construction

In a diversified portfolio, investment grade corporate bonds act as the income and stability counterweight to equities. During economic expansions, they outperform Treasuries (tighter credit spreads, income premium). During equity market stress, they partially cushion — though not as effectively as Treasuries, and far more effectively than high yield bonds.

Active Positioning: High Yield During Credit Spread Widening

For active investors, high yield corporate bonds create tactical opportunities during periods of credit spread widening. When recession fears spike HY spreads to 7-10%+ above Treasuries — as occurred in 2008-2009 and March 2020 — buying HY exposure through HYG or JNK at depressed prices captures both the high income and significant price appreciation as spreads normalise. This is an active, credit-cycle-aware strategy — not a passive income position.

Duration Management Across Rate Environments

Corporate bond exposure can be tailored to the interest rate environment through duration selection. In rising rate environments, shift toward short-duration IG corporate bonds (IGSB at ~0.04% ER) to reduce price sensitivity while maintaining income premium over Treasuries. As rates peak and begin declining, extend duration to longer-maturity IG bonds to capture price appreciation alongside income.

Tax Efficiency

Corporate bond interest income is taxed as ordinary income at both federal and state levels — a less favourable treatment than qualified dividends or long-term capital gains. Investors in high tax brackets (32%+) should calculate the after-tax yield of corporate bonds versus municipal bonds before allocating in taxable accounts. In tax-advantaged accounts (IRA, 401k), the tax treatment is irrelevant and corporate bonds’ higher pre-tax yield is fully retained.

Know the Spectrum Before You Buy

Corporate bonds are a legitimate, income-generating asset class with a range of risk/return profiles — but the investment merit depends entirely on where on the credit quality spectrum you are positioned.

The framework in brief:

- Investment grade corporate bonds (BBB-/Baa3 and above) → reliable income, low default risk, interest rate risk as primary concern; appropriate as portfolio stabiliser and income source

- High yield corporate bonds (below BBB-/Baa3) → equity-adjacent risk, meaningfully higher income, NOT defensive in equity bear markets; tactical rather than strategic allocation

- For most retail investors → ETFs (LQD for core IG, IGSB for short-duration IG, HYG/JNK for tactical HY) provide the most accessible, diversified, liquid route

- For investors with $50,000+ and willingness to conduct credit analysis → individual bonds provide certainty of par repayment at maturity and elimination of ETF NAV fluctuation risk

- Duration management → calibrate corporate bond duration to the interest rate environment; IGSB in rising rate periods; LQD or longer-duration in declining rate periods

Corporate bonds reward investors who understand the spectrum they are buying. Treating all corporate bonds as ‘safe income’ without attention to credit quality and duration is the most common and costly mistake in fixed income allocation.

| Build a Complete Fixed Income Strategy With ATGL

At AboveTheGreenLine.com we give investors the complete analytical framework for every asset class — from credit quality evaluation to duration management to corporate bond ETF selection. If you want the full system for building and managing your portfolio across every market environment, join us Above the Green Line. |

Frequently Asked Questions

What is the difference between corporate bonds and government bonds?

Corporate bonds are issued by companies; government bonds are issued by national governments (U.S. Treasuries, UK gilts, German Bunds). Government bonds from stable sovereigns carry essentially zero credit risk — the government can raise taxes or print currency to repay. Corporate bonds carry varying credit risk depending on the issuer’s financial health, requiring higher yields to compensate. The yield difference between a corporate bond and an equivalent-maturity Treasury is called the credit spread.

How do you make money from corporate bonds?

Corporate bond investors earn money in two ways: coupon income (fixed interest payments, typically semi-annual, paid throughout the bond’s life) and capital appreciation (buying a bond below face value in the secondary market, or benefiting from falling interest rates that push bond prices higher). Most retail investors focus primarily on coupon income, buying bonds or bond ETFs as income-generating portfolio components.

What is a good yield for corporate bonds?

Corporate bond yields move with market interest rates and reflect credit quality. In a 4-5% rate environment, investment grade corporate bonds typically yield approximately 1-2% above equivalent-maturity Treasuries (the credit spread). High yield bonds typically yield 3-6% above Treasuries in normal conditions, widening to 8%+ during credit stress. A ‘good yield’ is one that adequately compensates for the specific issuer’s credit risk relative to comparable alternatives.

What is the minimum investment for corporate bonds?

Individual corporate bonds have a face value of $1,000, but practical secondary market trading typically requires $5,000-$10,000 per bond for reasonable bid-ask spreads. Corporate bond ETFs — LQD for investment grade, HYG for high yield, IGSB for short-duration investment grade — have no minimum investment beyond the cost of a single share, making them the most accessible route for most individual investors.

Related Articles

[pt_view id=”fb2451fm3r”]