By Andrew Stowers

Updated June 16, 2026

An employee stock purchase plan with a 15% discount and lookback provision is one of the only places in financial markets where the minimum return is guaranteed before you know where the stock goes.

Most employees who have access to one don’t fully use it. Most who do participate don’t understand what determines their actual return or how to handle shares after purchase.

This guide covers the complete picture: plan mechanics, the lookback provision that amplifies returns in rising markets, how to calculate your actual gain, the tax treatment decision that can add thousands of dollars to your outcome, the hold-vs-sell framework every ESPP participant needs before their next purchase date, and the five mistakes that cost employees real money. For more information on how this all fits into stock trading within your portfolio, we highly encourage you to read over our Stock Trading Guide after finishing this article.

What Is an Employee Stock Purchase Plan?

| Quick Answer

An ESPP is a company-sponsored benefit allowing employees to purchase company stock at a discount — typically 5-15% — through payroll deductions over a defined offering period. Section 423 qualified plans offer the most favorable tax treatment if specific holding periods are met. The $25,000 IRS annual limit applies to qualified plans. |

When a company offers an employee stock purchase plan, it is giving employees the ability to buy its own stock at less than market price. The mechanism is simple: employees elect to have a percentage of their salary withheld each pay period, those deductions accumulate over an offering period, and at the end of each purchase period the plan automatically uses the accumulated funds to buy company stock at the discounted price.

Section 423 Qualified vs Non-Qualified Plans

The most important structural distinction is whether the plan qualifies under IRS Section 423. Section 423 qualified plans must be available to all eligible employees on equal terms, have a discount no greater than 15%, and provide the potential for favorable long-term capital gains tax treatment when shares are sold after meeting specific holding periods.

Non-qualified plans do not meet these requirements. The discount is recognized as ordinary income at the time of purchase — simpler tax treatment, but less favourable for employees in higher tax brackets.

ESPP vs Stock Options vs RSUs

These are three distinct equity compensation mechanisms. ESPPs: employee pays for shares at a discount through payroll deductions. Stock options: the right to buy shares at a predetermined price (the strike price) at a future date — no payment at grant. RSUs (Restricted Stock Units): shares granted to the employee subject to a vesting schedule — no purchase required. Each has different mechanics, tax treatment, and strategic implications.

IRS Limits and Eligibility

The IRS limits Section 423 plan purchases to $25,000 in company stock value per calendar year, based on the stock price at the beginning of the offering period. Part-time employees may be excluded, and employees already owning 5% or more of company stock are excluded from Section 423 plans.

How an ESPP Works: The Mechanics, the Lookback, and the Real Math

A typical Section 423 ESPP follows a six-step process from enrollment to share ownership:

- You enroll during an enrollment window and elect a payroll deduction percentage — typically 1-15% of salary

- Payroll deductions accumulate in a holding account throughout the offering period

- At the purchase date, the plan calculates your purchase price using the lookback provision

- The lookback selects the lower of: the stock price at the offering period start date OR the stock price at the purchase date

- A 15% discount is applied to that lower price — your actual purchase price

- Shares are purchased and deposited into your brokerage account

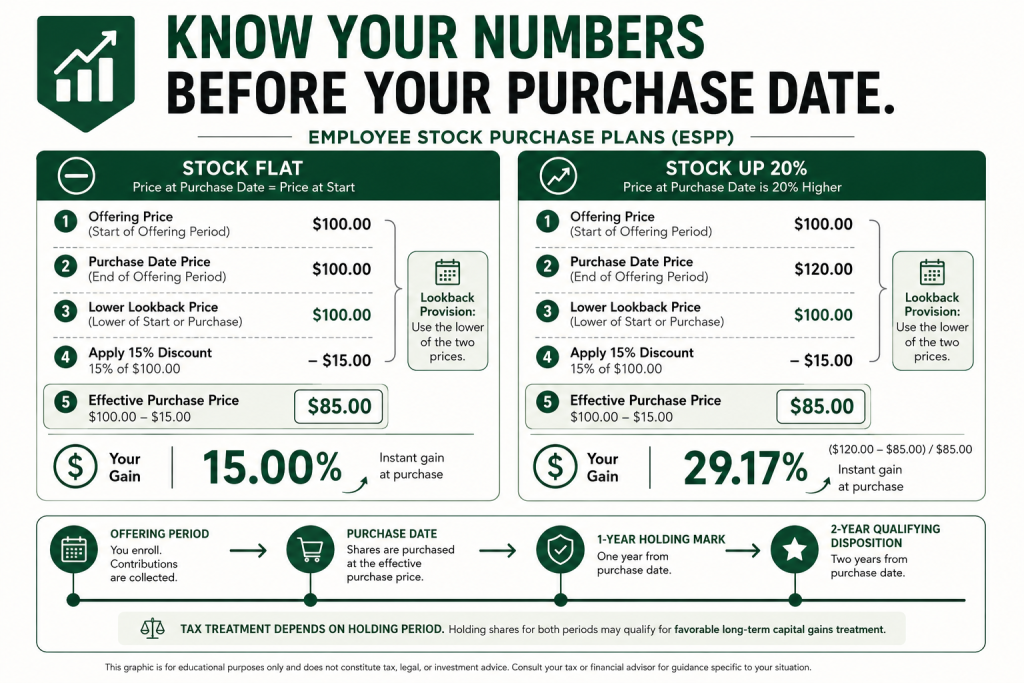

The Lookback Provision: Why This Feature Changes Everything

The lookback provision is the most valuable — and most underexplained — feature in a well-structured ESPP. Without it, you simply buy stock at a 15% discount to whatever the price is on purchase day. With it, you buy at a 15% discount to the lower of the offering period start price or the purchase date price.

In practice, this means two different scenarios work in your favor:

| Scenario | Stock Movement | Your Purchase Price | Immediate Gain |

|---|---|---|---|

| Flat stock | $100 start → $100 end | $85 (85% of $100) | $15 on $85 = 17.6% |

| Stock up 20% | $100 start → $120 end | $85 (85% of $100 start) | $35 on $85 = 41.2% |

| Stock down 12% | $100 start → $88 end | $74.80 (85% of $88) | $13.20 on $74.80 = 17.6% |

| Stock down 20% | $100 start → $80 end | $68 (85% of $80) | $12 on $68 = 17.6% |

The lookback protects you when the stock falls: your purchase price is 85% of the lower purchase-date price, still generating the same ~17.6% minimum gain on investment. The lookback rewards you when the stock rises: because you calculate from the (now lower) offering period start price, you capture a gain significantly larger than the basic 15% discount.

The Guaranteed Return: What Your ESPP Is Actually Worth

| The Math Most Employees Miss

A 15% discount does NOT mean a 15% return on your investment. You pay $85 for a $100 asset — your gain is $15 on an $85 investment, which equals 17.6%. Annualized over a 6-month offering period and sold immediately: approximately 35% annualized before tax. This is the guaranteed minimum floor for a flat stock. |

The fundamental calculation: Purchase price = $85. Immediate sale price = $100. Gain = $15. Return on investment = $15 ÷ $85 = 17.6%. Most employees think of the 15% discount as their return — but the correct frame is the gain on the money they actually invested.

The Annualized Return Frame

For a 6-month purchase period with an immediate sell: 17.6% in 6 months equates to approximately 35% annualized (compounded). For a 3-month purchase period: approximately 74% annualized. These are not projections — they are the mathematical outcome of the discount applied to the capital actually at risk.

When the Lookback Makes It Even Better

In a rising market scenario — stock at $100 at offering start, $120 at purchase date — the lookback buys at $85 (85% of the $100 start price). Selling at $120 immediately: $35 gain on $85 invested = 41.2% return in the purchase period. For a 6-month period: approximately 84% annualized. The lookback turns a rising market into an exceptional return amplifier.

The Only Loss Scenario

The only way to lose money with an immediate-sell ESPP strategy is if the stock falls more than the discount percentage from the purchase date price. With a 15% discount and lookback, a stock would need to fall from the offering period start price and continue falling on the purchase date before you can sell — a scenario that becomes less likely the more you monitor the stock and set immediate sell orders.

Compared to any guaranteed financial product — savings accounts, CDs, money market funds, government bonds — the guaranteed minimum return from a well-structured ESPP is unmatched.

ESPP Tax Treatment: Qualifying vs Disqualifying Dispositions

| Tax Advisor Note

ESPP tax treatment is complex and depends on individual circumstances. The following is a general educational overview. Consult a qualified tax professional for guidance specific to your situation and tax bracket. |

When and how you sell ESPP shares determines your tax bill. The IRS distinguishes between two types of sale, each with materially different treatment:

Qualifying Disposition: The Better Tax Outcome

To qualify for the more favorable tax treatment, you must meet BOTH conditions: (1) hold shares for at least 2 years from the offering period start date, AND (2) hold shares for at least 1 year from the purchase date. Both conditions must be met simultaneously — the two-year clock is the binding requirement for most employees since offering periods are often 6-24 months followed by a 1-year hold.

Under a qualifying disposition: the ‘bargain element’ — the lesser of (a) the actual discount percentage of the purchase price or (b) the stock’s appreciation from offering period start — is taxed as ordinary income. Any appreciation beyond the offering period start price is taxed at long-term capital gains rates (which are typically lower than ordinary income rates for most taxpayers).

Disqualifying Disposition: Simpler but Often More Expensive

A disqualifying disposition occurs when you sell before meeting either holding period requirement. The treatment: the bargain element (fair market value on the purchase date minus your discounted purchase price) is reported as ordinary compensation income on your W-2 in the year of sale. Additional appreciation above the fair market value on the purchase date is short-term or long-term capital gain depending on how long you held from the purchase date.

| Feature | Qualifying Disposition | Disqualifying Disposition |

|---|---|---|

| Hold Period Required | 2yr from offering + 1yr from purchase (BOTH) | Neither period met |

| Discount (Bargain Element) | Ordinary income (up to discount at offering start) | Ordinary income on W-2 in sale year |

| Additional Appreciation | Long-term capital gains (preferential rates) | Short or long-term cap gain |

| Employer W-2 Reporting | Ordinary income portion on W-2 | Full bargain element on W-2 |

| Overall Tax Burden | Generally lower (for appreciating stock) | Generally higher (more ordinary income) |

The Double-Taxation Trap — Read This Carefully

This is one of the most costly and common tax errors for ESPP participants. In a disqualifying disposition, your employer reports the bargain element as compensation income on your W-2. This automatically increases your adjusted cost basis for the shares.

If you sell at $150 and your original purchase price was $85, but the W-2 reports $15 of ordinary income (the bargain element), your adjusted cost basis is $100 — not $85. Your capital gain is $150 minus $100 = $50, not $150 minus $85 = $65.

Mistake: reporting a $65 gain when the correct figure is $50 — you would be paying capital gains tax on income already taxed as ordinary income on your W-2. This double-counting is a documented and common filing error. Check your brokerage 1099-B against your W-2 and adjust your cost basis accordingly — or work with a tax professional who understands ESPP transactions.

The Critical Decision: Should You Sell ESPP Shares Immediately or Hold?

This is the decision most ESPP content never clearly addresses. The right answer depends on your tax bracket, risk tolerance, and total employer stock concentration — but the framework is straightforward.

The Case for Selling Immediately

Selling at or very shortly after the purchase date captures the guaranteed discount return — approximately 17.6% minimum on flat stock, more on rising stock — eliminates all future single-stock risk on that position, and converts the ESPP from a stock market bet into a pure financial arbitrage.

The tax treatment (disqualifying disposition) is actually straightforward when understood correctly: the bargain element is ordinary income on your W-2 (expected and properly adjusting your cost basis), and any gain above your adjusted basis is short-term capital gain. For employees in moderate tax brackets, the immediate certainty of the gain often outweighs the potential tax savings from a qualifying disposition.

The Case for Holding to Qualifying Disposition

If the stock appreciates significantly during the qualifying holding period, the tax savings from long-term capital gains treatment on that appreciation can be meaningful — particularly for employees in higher income brackets where the difference between ordinary income rates and long-term capital gains rates is widest.

The hurdle: the stock must appreciate during the holding period, and you must tolerate full single-stock price risk throughout. A stock that falls 20% during the qualifying period erases the tax benefit of the qualifying treatment and creates a real economic loss on the invested capital.

The Concentration Risk Problem

The most underestimated risk for ESPP participants is employer stock concentration. Many employees simultaneously accumulate company stock through: ESPP purchases, RSU vesting, 401(k) employer match invested in company stock, and potentially stock options. The combined exposure to a single company’s performance can easily reach 30-50% of total net worth — a severe concentration for any single position, let alone a position that is also your income source.

The immediate-sell ESPP strategy directly addresses this: proceeds are redeployed into a diversified portfolio rather than added to an already concentrated employer position. For most employees, this is the financially prudent approach regardless of tax bracket.

Five ESPP Mistakes That Cost Employees Real Money

Mistake 1: Not Participating

An ESPP with a 15% discount and lookback provision guarantees a minimum positive return in most market conditions — a return that no savings account, certificate of deposit, or government bond matches. Not enrolling when eligible and cash flow allows is equivalent to turning down guaranteed compensation.

Mistake 2: Contributing Below the Maximum

If your financial situation allows maximum contributions, contributing less forfeits guaranteed return on available capital. Many employees set ESPP contributions at 5-10% when their plan and cash flow would support 15% (or the IRS $25,000 limit). Temporarily reducing discretionary spending to fund higher ESPP contributions is rational when the annualized guaranteed return is 30-40%+.

Mistake 3: Missing the Enrollment Window

Most Section 423 plans have specific enrollment windows — miss one, and you may wait 6-24 months for the next opportunity. Set a calendar reminder for every enrollment window in your plan. The cost of missing an offering period is the guaranteed return you could have earned.

Mistake 4: Allowing Concentration to Accumulate

Holding multiple rounds of ESPP shares alongside RSU grants and 401(k) employer stock match builds a concentrated single-stock exposure that can be devastating if the employer faces an adverse event. The 2001-2002 Enron collapse wiped out both retirement savings and employment for thousands of employees simultaneously — an extreme example of the concentration risk that accumulates when income and investment are tied to the same company.

Mistake 5: The Double-Taxation Error

After a disqualifying disposition, the bargain element appears as income on your W-2. This increases your cost basis for the sold shares. Failing to adjust the basis reported on your brokerage 1099-B — and instead calculating your capital gain from the original discounted purchase price — causes you to report and pay capital gains tax on income already captured on your W-2. This is one of the most commonly made ESPP tax errors and it is entirely preventable with careful recordkeeping and appropriate professional guidance.

How to Maximize Your ESPP Benefit: A Six-Step Action Plan

Regardless of where you are in the ESPP lifecycle — evaluating whether to enroll, actively contributing, or holding purchased shares — the following six steps apply:

- Step 1 — Review your plan documents and confirm enrollment status

Verify you are enrolled and contributing. If you are eligible but not enrolled, mark the next enrollment window in your calendar today.

- Step 2 — Set contributions to the maximum your cash flow allows

Determine the maximum your plan allows and whether your monthly cash flow supports it. If necessary, temporarily reduce discretionary spending during the offering period to fund higher contributions.

- Step 3 — Decide your sell/hold strategy before the purchase date — not after

Pre-deciding your approach eliminates emotional decision-making when you are watching the stock price move on purchase day. Most employees are better served by a default immediate-sell decision that they consciously override when qualifying disposition economics are compelling.

- Step 4 — Track key dates meticulously

For any shares you decide to hold: record the offering period start date, the purchase date, and the resulting qualifying disposition eligibility dates (2 years from offering start AND 1 year from purchase). A spreadsheet or calendar reminder for each qualifying date prevents inadvertent disqualifying dispositions.

- Step 5 — Execute sales promptly and adjust your tax basis correctly

For immediate sellers: set up a sell order for the day shares are credited to your account. When filing taxes, cross-reference your W-2 ordinary income from the ESPP bargain element with your 1099-B and adjust your cost basis to avoid double-taxation.

- Step 6 — Redeploy proceeds into a diversified portfolio immediately

ESPP proceeds should flow into a diversified investment account — not accumulated in cash and not reinvested into additional employer stock. This is the step that converts ESPP profit into sustainable long-term portfolio growth rather than concentrated employer stock exposure.

The ESPP Is Only as Valuable as How You Use It

An employee stock purchase plan with a 15% discount and lookback is genuinely one of the highest-return financial decisions available to corporate employees — a guaranteed minimum return that no savings vehicle or fixed income instrument matches. The structural advantage is real.

The summary:

- Understand the lookback: it turns rising markets into outsized gains and protects in falling markets

- Calculate correctly: 17.6% gain on $85 invested, not 15% — the distinction matters for decision-making

- Know your disposition type: qualifying requires BOTH 2 years from offering AND 1 year from purchase

- Default to immediate sell: captures the guaranteed return, eliminates stock risk, avoids concentration

- Watch the double-taxation trap: adjust your cost basis after a W-2 reports the bargain element

- Reinvest proceeds in a diversified portfolio — not back into employer stock

The employees who extract maximum value from their ESPP are those who treat the purchase date as an investment decision, not an automatic event — and who make deliberate choices about what happens to the proceeds.

| Build a Rules-Based Portfolio With ATGL

At AboveTheGreenLine.com we give investors the complete framework for every capital allocation decision — from maximizing ESPP benefits to building and managing a diversified, rules-based portfolio. Join us Above the Green Line and get access to the full system. |

Frequently Asked Questions

How much should I contribute to my ESPP?

For an ESPP with a 15% discount and lookback provision, most financial professionals recommend contributing the maximum allowed if cash flow permits — the guaranteed minimum return is difficult to match elsewhere. The IRS limits Section 423 plan purchases to $25,000 in stock value per year. Evaluate whether temporarily reducing discretionary spending during the offering period to fund maximum ESPP contributions makes sense given your personal cash flow situation.

What happens to my ESPP if I leave the company?

If you leave during an offering period, you typically receive a refund of your accumulated payroll deductions — you do not receive shares for any incomplete purchase period. Shares already purchased and credited to your account in prior purchase periods remain yours to manage. Some plans allow you to purchase shares with accumulated deductions upon departure; check your specific plan documents or HR portal for the exact terms.

Is an ESPP better than a 401(k)?

ESPPs and 401(k)s are not mutually exclusive and serve different purposes. A 401(k) with employer match should generally be funded at least to the full match first — the employer match is an immediate 50-100% return on contribution. After capturing the full 401(k) match, an ESPP with a 15% discount and lookback provision typically produces the next-best guaranteed return on additional savings, making it the logical priority for any remaining available contribution capacity.

What is the lookback provision in an ESPP?

The lookback provision calculates your purchase price based on the lower of the stock price at the offering period start date OR the purchase date — then applies the discount to that lower price. If the stock rose during the offering period, you buy at 85% of the (now lower) start price, creating a larger gain. If the stock fell, you buy at 85% of the (now lower) purchase date price, maintaining the standard discount. The lookback amplifies gains in rising markets and maintains the minimum discount protection in falling markets.

Related Articles

[pt_view id=”9517038dwu”]