By Andrew Stowers

Updated June 28, 2026

Bear markets are the environment where investment decisions made under pressure determine long-run outcomes far more than any individual stock pick made in a bull market.

The investor who panics and sells at the bottom, the investor who does nothing when they should reduce risk, and the investor who holds through a 40% drawdown without a plan — all make decisions that compound over decades. This guide provides the complete bear market investment framework: what to buy by asset class, which defensive tools work and which don’t, the specific instruments for active traders who want to profit from the decline, and the honest assessment of what to expect from each tool. After finishing this article, we encourage you to check out our Stock Trading Guide to frame how bear market investments fit into the bigger picture.

What Defines a Bear Market — and Why Strategy Must Change

| The Six Bear Market Investment Categories

(1) Treasury bonds and investment grade bonds, (2) Defensive sectors — utilities, consumer staples, healthcare, (3) Dividend stocks with reliable payment histories, (4) Gold and precious metals ETFs, (5) Cash and money market instruments, (6) Inverse ETFs — for active traders only. |

A bear market begins when a major stock index declines 20% or more from its most recent peak. Post-WWII U.S. bear markets have lasted an average of approximately 9-14 months and produced average peak-to-trough declines of approximately 35-40%. The shortest in modern history was the COVID crash in 2020 (approximately one month). The longest were the dot-com bear market (approximately 31 months) and the financial crisis (approximately 17 months).

Every bear market on record has been followed by a bull market that eventually exceeded the prior peak. This context — severe but time-limited decline followed by full recovery — shapes the correct investment response.

Why Bear Market Strategy Must Be Phase-Aware

The right positioning early in a bear market differs from the right positioning twelve months in. Early: reduce equity exposure if it exceeds your risk tolerance, increase defensive allocation. Mid-bear: maintain defensive positioning, avoid averaging into falling speculative names. Late bear: begin identifying recovery opportunities, consider extending equity duration.

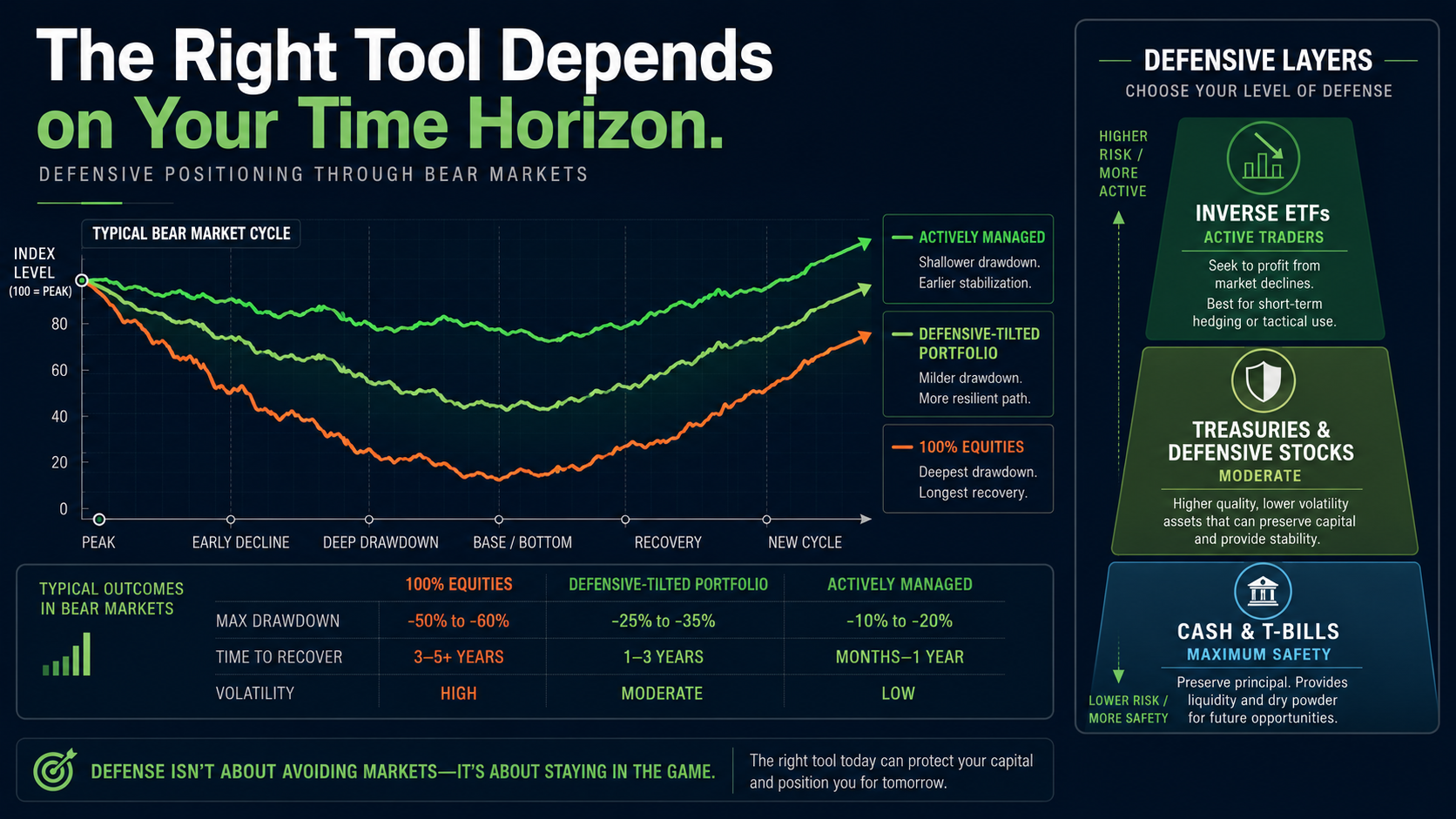

The Three Investor Profiles Framework

Passive long-term investors (time horizon 10+ years): time absorbs bear market losses; continuing contributions dollar-cost averages into lower prices; reducing equity allocation during a bear market typically produces worse outcomes than maintaining it.

Transition/near-retirement investors (5-15 years): sequence of returns risk is real; defensive buffers should be in place before the bear market arrives, not during it; the 2-3 year cash buffer allows equity portfolio to recover without forced sales.

Active traders: defined short positioning tools — inverse ETFs, put options, short selling — can produce profits during bear markets; requires strict rules, defined stops, and defined exit triggers.

The High-Yield Bond Warning

High-yield (junk) corporate bonds are NOT defensive in equity bear markets. They are highly correlated with equities during credit-stress events — their prices fell alongside equities in 2008-2009 and during the 2020 COVID crash. Only investment grade bonds and Treasury bonds provide reliable cushioning during equity market declines.

Defensive Sectors and Stocks: The Bear Market Stalwarts

Not all equity sectors fall equally in a bear market. Companies selling necessities, providing essential services, and maintaining earnings through economic downturns decline less than cyclical companies whose revenues are sensitive to economic conditions.

| Sector | Bear Market Behaviour | Key ETF | Approx. Yield | Why It Holds Up |

|---|---|---|---|---|

| Utilities | Typically outperforms | XLU | 3-4% | Regulated revenues; inelastic demand for electricity |

| Consumer Staples | Typically outperforms | XLP | 2-3% | Necessities (food, household); inelastic consumer spend |

| Healthcare | Typically outperforms | XLV | 1-2% | Inelastic demand for medicine/procedures |

| Financials | Mixed; banks are cyclical | XLF | 2-3% | Benefits from rates; hurt by credit losses |

| Energy | Depends on oil price | XLE | 3-4% | Uncorrelated to equity cycle; varies with commodities |

| Technology | Typically underperforms | XLK | 0.5-1% | High multiples compressed by rate rises; cyclical revenues |

The Utility Sector Caveat

Utilities are defensive on earnings but rate-sensitive on valuation — regulated utilities carry significant debt and pay high dividends, making them compete with bonds for yield-seeking capital. In rising-rate bear markets (2022), utilities underperformed despite defensive earnings because the rate increase reduced their relative appeal vs bonds. In recession-driven bear markets with falling rates, utilities are among the strongest performers.

Dividend Aristocrats as a Bear Market Quality Filter

Companies with 25+ consecutive years of dividend increases — dividend aristocrats — have demonstrated the financial durability to maintain payouts through every modern recession. This longevity is a quality signal: companies that raised dividends through 2001, 2008, and 2020 have proven earnings resilience that most growth stocks lack. ETFs like SCHD and VIG hold many dividend aristocrats and historically outperform broader market ETFs during bear markets by declining less.

Fixed Income in a Bear Market: Treasuries, Bonds, and Cash

Fixed income is the primary institutional bear market hedge — and the 2022 exception provides the most important recent lesson about when it works and when it doesn’t.

Treasury Bonds: The Traditional Safe Haven

In recession-driven bear markets, U.S. Treasury bonds are the most reliable equity portfolio cushion. When investors flee equities, they buy Treasuries — driving Treasury prices higher and yields lower. A portfolio holding TLT (20+ year Treasury ETF) alongside equities in a typical recession bear market experiences meaningful Treasury appreciation that partially offsets equity losses.

Duration matters for the magnitude: TLT (20+ year duration) gains the most when rates fall; IEI (intermediate, 3-7 year) provides moderate cushion; SHY (1-3 year) provides minimal price appreciation but capital preservation and some income.

The 2022 Exception — When Bonds Fail

The 2022 bear market was driven by inflation and aggressive Federal Reserve rate hikes — the opposite of a flight-to-safety recession scenario. Rising rates cause bond prices to fall. Both the S&P 500 (-20%) and AGG (the total bond market ETF, -13%) declined simultaneously. The 60/40 portfolio provided almost no cushioning because the shared driver — rising rates — was negative for both asset classes.

The 2022 solution was TIPS (Treasury Inflation-Protected Securities) and short-duration bonds. TIPS principals adjust for CPI inflation, protecting against the specific driver that hurt standard bonds. Short-duration bonds (SHY, IGSB) fell far less than long-duration bonds because their price sensitivity to rate changes is proportionally lower.

Cash: Maximum Flexibility, Inflation Cost

Cash and money market funds provide nominal capital preservation and the optionality to buy equities at bear market lows. In rising-rate bear markets (2022), cash yielding 4-5% as the Fed raised rates outperformed both stocks and bonds. In normal deflation-adjacent recessions, cash earns near-zero and underperforms Treasury bonds that appreciate on falling rates.

Gold and Commodities: Inflation Hedge and Portfolio Diversifier

Gold’s bear market role depends entirely on what is driving the bear market — and 2022 was gold’s most distinctive recent contribution.

Gold’s Bear Market Track Record

In the 2008-2009 financial crisis: gold fell initially in the liquidity-driven selloff (investors selling everything for cash), then surged over the following three years as monetary policy turned expansive. In the 2020 COVID crash: gold fell briefly in the liquidity event, then surged as QE expanded. In 2022: gold finished approximately flat — the most valuable diversification scenario, where both stocks and bonds declined while gold maintained value.

2022 was gold’s most important recent proof point: the specific environment where traditional portfolio diversification failed (stocks and bonds falling together), gold provided the diversification that the 60/40 framework could not.

IAU and GLD: The Gold ETF Vehicles

IAU (iShares Gold Trust, ~0.25% ER) and GLD (SPDR Gold Shares, ~0.40% ER) are the two largest physically-backed gold ETFs. Both track spot gold with minimal tracking error. IAU’s lower expense ratio makes it preferable for long-term holders. One critical tax note: gold ETFs are classified as collectibles — long-term capital gains are taxed at a maximum rate of 28%, not the 20% maximum for stocks. Hold in a Roth IRA or traditional IRA to eliminate this disadvantage.

Broader Commodities in Bear Markets

DBC (Invesco DB Commodity Index Tracking Fund) and PDBC (actively managed commodity futures) provide exposure to energy, metals, and agricultural commodities. In commodity-driven inflationary bear markets (2022), commodity ETFs significantly outperformed both equities and bonds — oil prices rose dramatically while stock prices fell. In demand-destruction recessions (2008), commodities fell alongside equities.

Inverse ETFs and Short Strategies: For Active Traders Only

| Important Warning

Inverse ETFs are NOT long-term bear market holdings. Daily rebalancing creates compounding decay that can produce losses even when the underlying index declines over a multi-month period. They are short-term tactical instruments for active traders — not defensive replacements for bonds or gold. |

How Inverse ETFs Work

Inverse ETFs use derivatives to deliver the negative of an index’s daily return. SH (ProShares Short S&P 500) delivers approximately -1x the S&P 500’s daily return. SDS delivers -2x. SQQQ delivers -3x the Nasdaq-100. On a day when the S&P 500 falls 2%, SH rises approximately 2% and SDS rises approximately 4%.

The Compounding Decay Problem

The daily rebalancing creates a mathematical drag that compounds over time. Example: an index falls 10% then rises 10% — the index is approximately -1% from its starting point. A -2x leveraged inverse ETF falls approximately 20%, then needs to rise approximately 25% to recover to breakeven — the asymmetry of compounding losses creates decay. In a volatile, choppy bear market, a leveraged inverse ETF can lose money even if the index ultimately ends lower.

The longer the hold, the worse the decay. Inverse ETFs held for days to a few weeks during a confirmed downtrend can be effective; held for months through a bear market with bounces, they typically underperform expectations dramatically.

Short Selling and Put Options

Short selling individual stocks or ETFs provides similar bear market exposure to inverse ETFs without the daily rebalancing issue. Buying put options defines risk to the premium paid — maximum loss is the option premium. Both require more sophistication than inverse ETFs but are cleaner in structure for longer-duration bearish positions.

What to Avoid in a Bear Market

High-Yield Bonds (The False Defensive)

The most important ‘must avoid’: HYG, JNK, and other high-yield bond ETFs decline alongside equities in bear markets driven by credit concerns. In 2008-2009, high-yield bonds fell 35-40% alongside equities. Adding HYG to a portfolio for ‘income protection’ in a bear market provides neither income security nor capital protection when credit conditions deteriorate.

Panic Selling at Market Lows

Investors who sold S&P 500 positions at the March 2009 low (approximately 57% below the 2007 peak) and re-entered at the prior high missed the entire 400%+ bull market that followed. Bear markets end; the recovery begins before the all-clear signal is obvious. Investors waiting for confirmed recovery typically re-enter 20-30% above the actual trough, having locked in permanent losses and missed the sharpest recovery gains.

Leveraged Long ETFs (TQQQ, UPRO)

The same compounding decay that hurts inverse ETFs in volatile markets destroys leveraged long ETFs during bear markets. TQQQ (3x Nasdaq-100) declined approximately 80% from its 2021 peak to its 2022 trough — far more than the approximately 35% Nasdaq-100 decline because leveraged compounding amplifies sequential daily losses asymmetrically.

Averaging Into Speculative Positions

Buying more of a speculative growth stock that has already fallen 50% is not value investing — it is conviction in a company that may not survive the bear market. Distinguish between quality large-cap companies worth purchasing at lower prices (Apple, Microsoft, McDonald’s — companies with durable competitive advantages and strong balance sheets) and speculative companies without profitability whose valuations relied on perpetually cheap capital.

The ATGL Rules-Based Bear Market Framework

A rules-based bear market framework replaces reactive decisions made under pressure with pre-defined responses to specific market conditions.

Passive Long-Term Investor Playbook

Determine the maximum equity drawdown you can psychologically sustain without forced selling — and hold it. Continue regular contributions throughout the bear market. A 40% allocation to equities through a 40% bear market means the equity portion falls 16% of total portfolio value — survivable without panic. A 90% allocation through the same bear market falls 36% of portfolio — many investors cannot hold that without selling at the worst time.

Transition/Near-Retirement Investor Playbook

The 2-3 year cash and short-term bond buffer should be established during the transition phase — before the bear market. During the bear market: draw spending from the cash buffer, not from the equity portfolio. The equity portfolio has time to recover without forced liquidation. Maintain defensive sector tilt (XLU, XLP, XLV) within equity allocation.

Active Trader Playbook

Bear market confirmation signals: sustained negative market internals (TICK consistently below -400, ADD consistently negative), price below declining 50-day and 200-day moving averages, death cross (50-day crossing below 200-day). Entry on failed rallies to declining moving averages. Exit when market internals show sustained improvement and price begins reclaiming key moving average levels.

Re-Adding Risk: The Recovery Signal Framework

- Breadth improvement: advance-decline line stabilising or improving after the bear market low

- Price action: successful retest of the bear market low with positive divergence in MACD

- Market internals: TICK and ADD returning to neutral-to-positive territory on sustained basis

- Moving average reclaim: price reclaiming 50-day moving average on above-average volume

The Plan Is More Valuable Than the Assets

Bear markets test every investor’s discipline. The tools exist: Treasury bonds for recession-driven declines, TIPS and short-duration bonds for rate-driven declines, gold for inflation and diversification, defensive sectors for equity allocation, inverse ETFs for active traders. The correct selection depends on the type of bear market — not a single universal defensive playbook.

The summary:

- Investment grade bonds and Treasuries: primary defensive tool in recession-driven bear markets

- TIPS and short-duration bonds: the 2022 lesson — inflation-driven bear markets require a different fixed income response

- Defensive sectors (XLU, XLP, XLV): decline less than the broad market; maintain dividend income

- Gold (IAU): provides diversification when both stocks and bonds fail together (2022 proof point)

- Cash: maximum preservation and flexibility; the right call in rising-rate bear markets

- Inverse ETFs (SH, SDS): for active traders holding days to weeks only — NOT long-term defensive holds

- Avoid: HYG/JNK (not defensive), panic selling, leveraged long ETFs, averaging into speculative positions

| Navigate Every Market Cycle With ATGL’s Rules-Based System

At AboveTheGreenLine.com we give active investors the complete framework for every market environment — bull, bear, and transition — with defined signals, positioning rules, and risk management that removes emotional decision-making from the equation. Join us Above the Green Line. |

Frequently Asked Questions

Where should I put my money during a bear market?

Capital typically flows to three defensive categories in equity bear markets: U.S. Treasury bonds (prices rise in flight to safety), defensive equity sectors (utilities, consumer staples, healthcare — earnings are less cyclical), and gold as a non-correlated diversifier. In rising-rate bear markets specifically (2022), TIPS and short-duration bonds outperformed standard bonds. Cash provides maximum preservation and flexibility to buy at lower prices. The appropriate allocation depends entirely on your time horizon and the bear market’s underlying cause.

How long do bear markets last?

Post-WWII U.S. bear markets have lasted approximately 9-14 months on average. The shortest was the 2020 COVID crash (approximately 1 month). The longest were the 2000-2002 dot-com bear market (approximately 31 months) and the 2007-2009 financial crisis (approximately 17 months). Bear markets are significantly shorter than the bull markets that follow them — a key context for investors deciding whether and how much to reduce equity exposure.

Should I sell stocks during a bear market?

Selling stocks at bear market lows locks in losses and risks missing the recovery. Investors who sold at the March 2009 S&P 500 low and waited for confirmation of recovery missed most of the 400%+ subsequent bull market. For investors with 10+ year time horizons, maintaining equity exposure and continuing contributions through the bear market is typically the optimal long-run strategy. For investors in or near retirement, having a defined defensive allocation in place before the bear market is more effective than reactive selling during it.

Are inverse ETFs good during a bear market?

Inverse ETFs can produce gains in a bear market for active traders holding for days to a few weeks. For longer holds, daily rebalancing creates compounding decay — in a volatile bear market with bounces, a leveraged inverse ETF can lose money over the full period even if the index ultimately falls. SH (1x inverse S&P 500) is the most conservative inverse option. All inverse ETFs are tactical short-term instruments, not buy-and-hold defensive alternatives to bonds or gold.

Related Articles

[pt_view id=”9517038dwu”]