By Andrew Stowers

Updated June 16, 2026

Day trading options is not simply day trading stocks with more leverage. Options have non-linear price behavior governed by the Greeks — and near expiration, gamma makes options move in ways that can generate extraordinary returns on correct directional calls and wipe out entire positions on small adverse moves.

Understanding how the Greeks behave in an intraday context, why 0DTE options are a fundamentally different instrument from standard options, and how to size positions so that a wrong trade does not end your trading day: this is what separates profitable options day traders from the majority who lose. This guide provides the complete framework.

How Day Trading Options Differs From Trading Stocks — and From Options Investing

| The 100% Loss Reality

A long option can lose its entire premium value in a single trading session. This is categorically different from stock day trading where a $5,000 stock position losing 10% loses $500 — not its entire value. Intraday options traders must size positions knowing that 100% premium loss is a realistic, routine outcome on individual trades. |

Options Day Trading vs Stock Day Trading

Stock day trading provides linear price exposure — a $1 move in a $50 stock changes the position value by $1 per share. Options day trading provides non-linear exposure: the same $1 move in the underlying might move an at-the-money option $0.50 (delta 0.50), but as the underlying approaches the strike price, that delta can spike toward 0.90 — the position profits exponentially faster on continued movement. This acceleration (gamma) is the defining feature of near-expiration options.

Options Day Trading vs Options Investing

Multi-week options positions allow time for the investment thesis to develop — the trader tolerates short-term price fluctuations and manages theta (time decay) as a gradual cost. Day trading options collapses this entirely: the entire window is one trading session. Direction, timing, and magnitude all have to be right within hours. There is no ‘wait for the trade to work’ — only act or exit.

The Pattern Day Trader Rule

In U.S. margin accounts, the SEC’s pattern day trader rule requires $25,000 minimum account equity for traders who execute 4 or more day trades in a 5-business-day rolling period. Below $25,000, a maximum of 3 day trades per 5-day period is permitted. Most active options day traders maintain $25,000-$50,000+ to operate without these restrictions and to absorb normal losing streaks without account risk.

The Options Greeks Every Day Trader Must Understand

Four Greeks govern options pricing and P&L. For day trading, their relative importance differs significantly from multi-week options positions.

| Greek | What It Measures | Intraday Relevance | Primary Risk/Use |

|---|---|---|---|

| Delta | Option price change per $1 underlying move | Primary directional exposure measure | Choose strike based on desired delta exposure |

| Gamma | Rate of delta change — delta acceleration | Critical: dominates near-expiration options | Amplifies gains AND losses near expiration |

| Theta | Daily time value decay | Less urgent intraday; extreme in final hours for 0DTE | Erodes all bought options value over time |

| Vega | Sensitivity to implied volatility change | Important for event-driven trades (earnings, Fed) | IV crush can negate correct directional calls |

Delta: Your Directional Exposure

Delta measures how much the option price moves per $1 move in the underlying. A 0.50 delta call gains approximately $0.50 for every $1 rise in the underlying. Deep in-the-money options approach delta 1.0 — near-equivalent to holding 100 shares of stock. At-the-money options typically carry delta ~0.50. Higher delta = higher cost, lower leverage ratio; lower delta = cheaper premium, higher leverage, more likely to expire worthless.

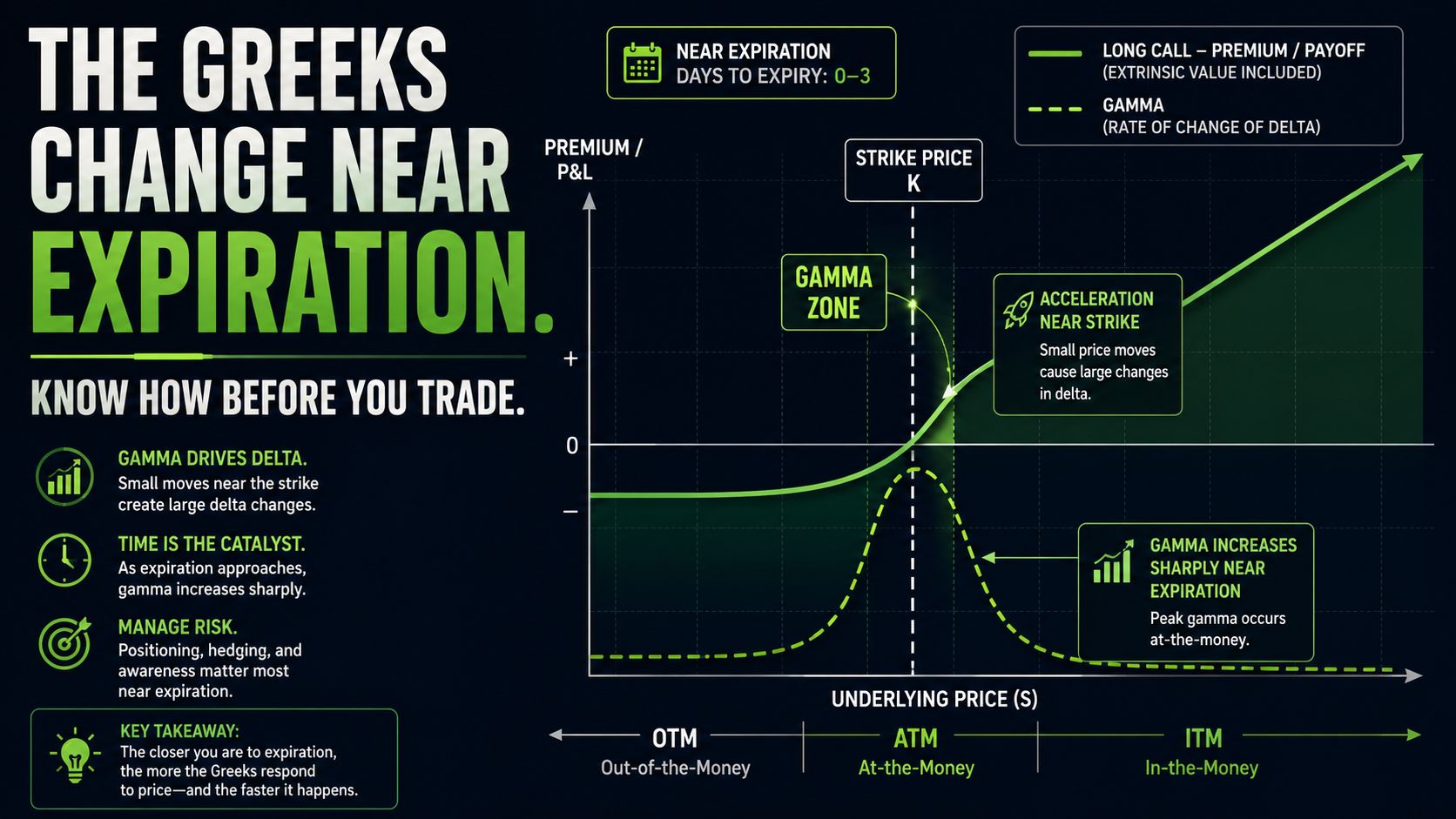

Gamma: The Intraday Acceleration Factor

Gamma is the most important Greek for day trading options. It measures how fast delta changes when the underlying moves. When gamma is high — which occurs for near-expiration, at-the-money options — a $1 move in the underlying can change your delta from 0.50 to 0.80. The next dollar move profits more than the first; the dollar after that profits more still.

Numerical example: a 0DTE SPY call with delta 0.40 and gamma 0.15 on a $5 underlying move toward the strike: delta becomes 0.40 + (5 × 0.15) = 0.40 + 0.75 → capped at 1.00. The option that paid $0.10 might be worth $2.00-$3.00 on a sharp move. The same gamma works against you on adverse moves.

IV Crush: The Event-Driven Trap

Before high-profile events — earnings announcements, Federal Reserve decisions, major economic data — implied volatility expands as uncertainty premium is priced into options. After the event, IV collapses rapidly (IV crush). A trader who bought calls before earnings with a correct directional view may still lose money if the IV crush reduces the option value faster than delta appreciation adds it. Day traders using options around events must understand this dynamic.

Choosing Your Day Trading Options Universe: Liquidity First

| The Bid-Ask Spread Math

A SPY option with a $0.02 bid-ask spread on a $1.00 premium costs approximately 2% per round trip (entry + exit). An illiquid option with a $0.20 bid-ask spread on the same premium costs 20%. In day trading where profit targets may be 20-50% of premium, wide spreads eliminate edge entirely. |

SPY Options: The Day Trader’s Primary Market

SPY options are the most liquid equity options market in the world. They offer: multiple weekly expirations (Monday, Wednesday, Friday), tight bid-ask spreads on near-the-money strikes ($0.01-$0.03 on liquid strikes), enormous volume that ensures reliable execution, and a deep options chain covering a wide range of strikes. For most options day traders, SPY is the primary instrument.

SPX Options: The Advanced Alternative

SPX (S&P 500 Index) options are European-style (no early assignment risk) and cash-settled. The most important benefit: under Section 1256 of the U.S. tax code, SPX options (as broad-based index options) are taxed at 60% long-term / 40% short-term capital gains rates regardless of holding period. For active day traders with high trading frequency, this 60/40 treatment can be meaningfully more favourable than short-term capital gains treatment on SPY options. Verify with a tax professional. SPX is priced at 10x SPY, requiring more capital per contract.

Individual Stocks on Catalyst Days

Stocks with earnings releases, FDA approvals, or major news events see IV expansion before the catalyst and high volume throughout. These are tradeable with options but require understanding IV crush risk. Stick to large-cap stocks with liquid, tight-spread options chains. A stock with wide bid-ask spreads in its options chain on a normal day will be even worse on catalyst days when bid-ask widens further.

The Three Core Day Trading Options Strategies

Strategy 1: Long Directional Calls and Puts

The most straightforward intraday options approach: buy a call or put with a strike near the current underlying price (delta 0.40-0.60) when a strong directional move is expected. Enter with market internals confirmation — for calls: TICK above neutral (+200 or better), price above VWAP, MACD histogram expanding bullishly, volume confirming the move. Profit target: typically 20-50% of premium. Hard stop if premium falls 20-30% from entry.

This strategy works best in trending, high-volatility market environments. In choppy, low-volatility markets, theta and bid-ask spread erosion reduce the expected value of buying options intraday.

Strategy 2: Vertical Debit Spreads

A debit spread buys an option near the current price and sells a further out-of-the-money option at the target price. This reduces the cost of the long option while defining both maximum profit and maximum loss.

Bull call spread: buy the $450 SPY call, sell the $455 call. Maximum loss = net premium paid. Maximum profit = the spread width minus net premium. The spread costs less than the outright long call and has defined risk — no 100% loss beyond the net debit. Appropriate for traders who want directional exposure with lower capital at risk per trade.

Strategy 3: Near-Expiration Gamma Scalping

Trading 0DTE or 1DTE options specifically to exploit gamma acceleration on strong directional moves. Very short hold times (5-30 minutes). Small premium entry ($0.05-$0.30 per contract). High reward/risk ratios when the trade works (5:1, 10:1, or more on strong moves). Requires the strictest entry discipline — only trade with a clear catalyst, VWAP and market internals confirmation, and immediate exit if no follow-through within the first few minutes.

0DTE Options: The Most Aggressive Intraday Approach

| Important Warning

0DTE options are the highest-risk intraday options instrument available. Positions routinely go to zero. The strategy requires a statistically demonstrated edge — a pattern that has worked consistently with documented positive expected value — not a feeling about market direction. |

0DTE (zero days to expiration) options expire on the same day they are traded. SPY has Monday, Wednesday, and Friday expirations; SPX has the same schedule plus occasional daily expirations. This availability makes true intraday 0DTE trading possible throughout the week.

The Extreme Gamma Profile

A 0DTE SPY call with strike $5 above current price might trade for $0.10 at 10am. If SPY moves $3 toward the strike by 11am, that option might be worth $0.30. If SPY moves the full $5 to the strike, the option might be worth $1.50-$3.00 — a 15-30x return on the premium. The same gamma that creates these returns creates complete premium loss on any trade that does not work quickly. A 0DTE option that is out of the money at 3:45pm is worth essentially zero.

0DTE Position Sizing

Size 0DTE positions so that a 100% premium loss on any individual trade is a small, acceptable portion of your total daily risk. If your maximum per-trade loss is $200 and a 0DTE option costs $0.10 per contract, maximum position is 20 contracts ($200 ÷ ($0.10 × 100) = 20). This calculation forces appropriate sizing before every 0DTE entry.

Time of Day Matters

Morning (9:30-11:30am): highest intraday volatility; gamma moves are most responsive to market internals; best conditions for 0DTE directional trades on opening drive setups.

Midday (11:30am-1:30pm): lower volatility, less reliable signals; many experienced traders reduce or eliminate new 0DTE entries during this period.

Final 30 minutes (3:30-4:00pm): extreme gamma; even small underlying moves cause massive option value changes in both directions; most experienced 0DTE traders avoid new entries in the final 30 minutes due to unpredictable directional swings.

Risk Management and Position Sizing

Risk management for options day trading requires more explicit rules than stock day trading because the loss magnitude is different — a single options position can lose 100% of premium.

The Per-Trade Maximum Loss

Define your maximum acceptable dollar loss per trade before entry. Formula: max contracts = max loss per trade ÷ (premium × 100). For a $0.25 option with $300 max loss per trade: 300 ÷ 25 = 12 contracts maximum.

This calculation must happen before every trade. Sizing based on ‘how many contracts do I want to own’ — rather than on a defined maximum dollar loss — is the primary position sizing error in options day trading.

Daily Loss Limit

Define the maximum daily loss that triggers a full stop-trading decision. Typically 2-3% of trading account. When this limit is hit — regardless of how confident you feel about the next trade — trading stops for the day. The psychology of trying to recover a daily loss by taking more risk is one of the most consistent account-destroying patterns in options day trading.

The Overnight Close Rule

All intraday options positions close before market close — without exception, unless the position was explicitly entered as a multi-day trade with overnight risk deliberately accounted for. Short-dated options (0DTE, 1DTE) held overnight face gap risk with no ability to manage the position during the gap. The potential loss from an adverse overnight gap on a short-dated option can be the entire premium.

Tools, Setup, and the Honest Reality of Day Trading Options

Brokerage Requirements

Options day trading requires Level 2 approval (buying calls and puts) at minimum; Level 3 approval (spreads) for debit spread strategies. Obtain the appropriate approval level before the trading session. Major platforms suited to active options day trading: thinkorswim (TD Ameritrade/Schwab), Tastytrade, Interactive Brokers, TradeStation. These platforms display real-time Greeks, options chains with volume and open interest, and integrate with market internals data.

Open Interest and Liquidity Verification

Before entering any options day trade, verify that the specific contract has adequate open interest and volume for reasonable execution. The open interest at each strike indicates existing participant positions — higher open interest generally correlates with tighter bid-ask spreads and better execution.

Tax Considerations

Standard options trades (SPY, QQQ, individual stocks) closed intraday are short-term capital gains — taxed at ordinary income rates. SPX index options are Section 1256 contracts under U.S. tax code, taxed at 60% long-term / 40% short-term rates regardless of holding period — potentially more favorable for active traders. Verify with a qualified tax professional as regulations change.

The Honest Reality

The majority of retail options day traders lose money. The primary causes: trading without a statistically demonstrated edge, over-sizing positions relative to account capital, holding losing trades hoping for recovery, and not respecting the daily loss limit. Options day trading is a high-skill discipline with a long learning curve. A realistic progression: study the mechanics thoroughly, paper trade to build pattern recognition, start with very small real-money positions, scale up only after 3-6 months of documented profitable results.

A Systematic Approach to Day Trading Options

Day trading options rewards the systematic, rules-based trader — the one who defines every entry criterion, every exit rule, every maximum loss, and every position size before the market opens, then executes those rules without emotional override.

The framework:

- Gamma accelerates near expiration — the defining intraday Greek; understand it before trading 0DTE

- SPY for liquidity and simplicity; SPX for potential Section 1256 tax advantage (verify with tax professional)

- Three strategies: long calls/puts for momentum, debit spreads for defined risk, near-expiration scalping for gamma exposure

- 0DTE: size so 100% premium loss is acceptable; trade morning momentum, avoid the final 30 minutes

- Per-trade max loss formula: max contracts = max loss ÷ (premium × 100); calculate before every entry

- Daily loss limit: define it, then honor it completely

- Overnight close rule: all intraday options positions close before market

- The honest reality: this requires documented edge, strict discipline, and a willingness to lose money in the learning phase

| Apply a Rules-Based System With ATGL

At AboveTheGreenLine.com we give active traders the complete systematic framework — from market internals filters to position sizing to entry and exit rules — that makes trading options intraday a disciplined process rather than a gamble. Join us Above the Green Line. |

Frequently Asked Questions

How much money do you need to day trade options?

The SEC’s pattern day trader rule requires $25,000 minimum account equity for accounts executing 4 or more day trades in a 5-business-day period in a U.S. margin account. Below $25,000, traders are limited to 3 day trades per 5-business-day rolling period. Most active options day traders maintain $25,000-$50,000+ to operate without PDT restrictions and to size positions appropriately relative to normal losing streaks.

What is a 0DTE option?

A 0DTE (zero days to expiration) option expires on the same day it is traded. SPY, SPX, and QQQ have options expiring multiple days per week, making true same-day 0DTE trading possible throughout the week. 0DTE options have extreme gamma (small underlying moves cause large option value changes), very low absolute premium, and go to zero or near-zero by market close if out of the money. They are the most aggressive intraday options instrument available.

What options are best for day trading?

For day trading, the most important criterion is liquidity — specifically, tight bid-ask spreads and high volume. SPY options (S&P 500 ETF) are the most liquid equity options market with multiple daily expirations and spreads of $0.01-$0.03 on near-the-money strikes. SPX (S&P 500 Index) options offer similar liquidity with potentially favorable Section 1256 tax treatment. Individual stock options on catalyst days can be traded but require larger bid-ask spreads and higher volatility awareness.

Is day trading options profitable?

Day trading options can be profitable for traders with a defined statistical edge, strict risk management, and the capital to sustain normal losing streaks. The vast majority of retail options day traders lose money — primarily from trading without a defined edge, over-sizing positions relative to account capital, and not honoring daily loss limits. The mechanics and Greek behavior are learnable; the discipline to follow rules under pressure is the actual differentiator between profitable and unprofitable options day traders.

Related Articles

[pt_view id=”9b64b383ox”]