By ATGL

Updated August 28, 2025

Options allow you to express a view on direction, volatility, and time. Spreads refine that view by balancing cost and risk. A calendar spread uses the same strike and underlying, but different expirations. It is designed to take advantage of time decay differences and changes in implied volatility. This guide explains how calendar spreads work (calls and puts), what drives performance, how to structure trades, and how to manage positions if the underlying moves unexpectedly. Where helpful, we reference primers from Investopedia, tastylive, Option Alpha, and Saxo.

How a Calendar Spread Works in Options Trading

Definition (time difference): A calendar spread combines one short option in a nearer expiration with one long option in a later expiration, at the same strike on the same underlying. You can construct calendars with calls or puts.

- Risk/reward overview:

- Long calendar (most common): enter for a net debit; risk is limited to that debit. You want the underlying to be near the strike as the short leg approaches expiration, and/or implied volatility (IV) to increase for the back-month option.

- Short calendar: enter for a net credit; vega negative and theta negative. This structure benefits if back-month IV falls or the underlying moves away from the strike such that both options decay efficiently. Risks can be higher than the credit received.

Long Calendar Spread Explained

- Construction: Buy longer-dated option (e.g., 60–90 days), sell shorter-dated option (e.g., 20–30 days), same strike. Calls or puts may be used.

- Typical outlook: Neutral to slightly directional toward the strike. You prefer front-month decay to outpace back-month decay, and IV stability or expansion in the longer option.

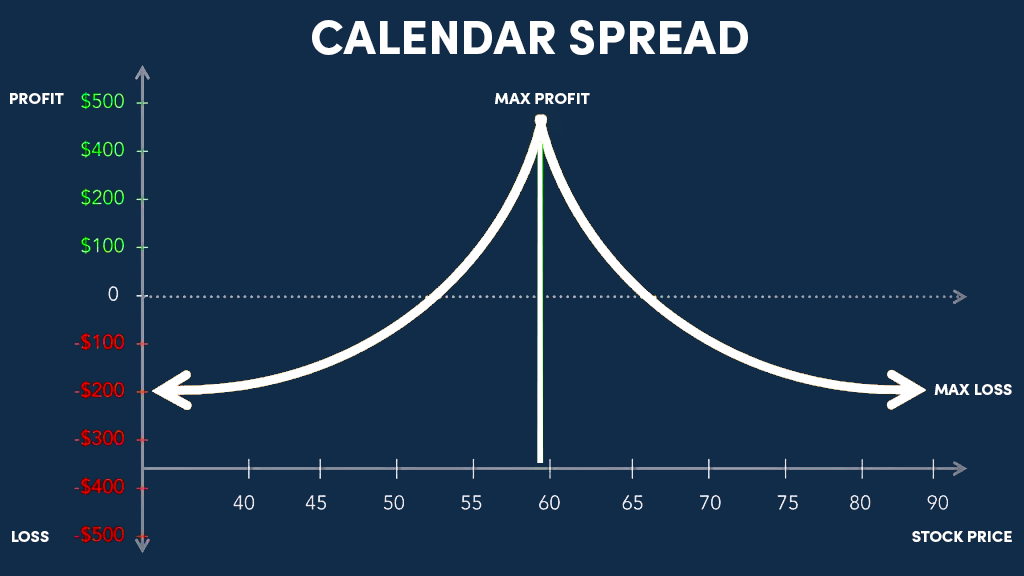

- Payoff profile: Peak theoretical value when price pins the strike near the short leg’s expiration; maximum loss is the net debit.

- Example (SPY): With SPY near 500, buy the 500 call 60 DTE, sell the 500 call 25 DTE. If SPY hovers near 500, the short call decays faster; you can buy it back cheaper, then either hold the back-month long call or roll into a new calendar.

- Operational notes: Watch earnings/major events that may spike or crush IV; monitor assignment risk into the short leg’s expiration, especially if it goes in-the-money.

Short Calendar Spread Explained

- Construction: Sell longer-dated option, buy shorter-dated option, same strike (entered for a credit).

- Typical outlook: Expect back-month IV to contract or the price to move away from the strike so both options decay.

- Risk profile: Vulnerable to IV expansion and sticky movement near the strike; adverse moves can increase the net value of the longer-dated short option.

- Use case: More advanced; often employed around expected IV crush in the back month or to position against mean-reverting volatility.

FAQ — What is the “calendar spread rule”?

A calendar spread uses identical strikes and underlying but different expirations. In most broker platforms the long calendar is entered for a debit with defined risk (the debit). Trading permissions, margin, and exercise/assignment rules apply; confirm with your broker.

Key Factors That Influence Calendar Spread Performance

Calendar outcomes depend on time decay (theta), implied volatility (vega), and underlying movement (delta and gamma).

- Theta: The short, near-term option typically decays faster than the long, later-dated option. Long calendars benefit from this differential.

- Vega: The longer-dated option carries more vega. Long calendars benefit when IV rises or remains bid; short calendars benefit when IV falls.

- Price path: Staying near the strike into the short leg’s expiration is favorable for long calendars; a large move away from the strike reduces value.

FAQ — Are calendar spreads profitable?

They can be if time decay works in your favor and IV does not fall sharply against your back-month long option. Profitability also depends on entry price, strike selection, volatility regime, and management. In quiet markets with stable or rising IV, long calendars often perform well; in fast, directional markets with IV compression, results can degrade.

Role of Time Decay and Volatility

- Time decay: Expect to benefit from the short leg’s faster decay if price stays near the strike. If price drifts far, both legs lose value.

- Volatility: Before entry, benchmark IV using tools like our overview of implied volatility. Long calendars prefer cheap to fair IV with potential to rise; short calendars prefer rich IV with room to fall.

- Ticker selection: High-liquidity underlyings (e.g., SPY, AAPL) typically offer tighter markets and more predictable behavior than thin, event-driven names.

Calendar Spread Strategy: Setting Up Trades

Market outlook and typical setup

- Neutral/mean-reverting view: Use a long calendar at-the-money (ATM).

- Mildly bullish: Use a long call calendar slightly OTM (above price).

- Mildly bearish: Use a long put calendar slightly OTM (below price).

- Short calendar: Consider only if you have a strong reason to expect IV contraction and a move away from the strike; understand the added risks.

Step-by-step (long calendar)

- Choose the underlying: Favor liquid names with tight markets (e.g., SPY, AAPL).

- Select expirations: Short leg ≈ 20–30 DTE; long leg ≈ 50–90 DTE.

- Pick the strike: Start ATM for neutral; shift one strike OTM for a mild directional bias.

- Price the spread: Confirm a reasonable debit relative to expected decay and IV.

- Place the order: Enter as a single calendar order ticket to control slippage.

- Risk parameters: Define maximum loss (the debit) and conditions for early exit (e.g., IV crush, big directional move).

- Management: If price pins the strike as the short leg decays, consider buying back the short, then either:

- roll the short to a later front-month (same strike) to create a rolling calendar, or

- close the position if the long leg’s value is maximized relative to remaining risk.

If the market moves

- Trend away from the strike: Consider shifting the strike (close and reopen at a more appropriate strike), or convert to a diagonal (roll the short leg to a strike closer to current price).

- IV crush (e.g., post-earnings in back month): Long calendars lose vega; reduce exposure or close if thesis has changed.

- Approaching short-leg expiration: Manage assignment risk, especially if the short is in-the-money. Many traders close or roll the short before expiration day to avoid unwanted stock positions.

FAQ — Is a calendar spread bullish or bearish?

A calendar can be neutral, slightly bullish, or slightly bearish depending on strike placement (ATM/OTM) and call vs. put choice. The classic ATM long calendar is market-neutral with positive vega.

Pros and Cons of Using Calendar Spreads

Pros

- Defined risk (long calendars): Max loss is the net debit.

- Flexible bias: Neutral to mildly directional via strike selection and call/put choice.

- Vega exposure: Can benefit from IV expansion in the longer-dated option.

- Income potential through rolls: Re-selling front-month options against the same long can generate additional credits over time.

Cons

- Sensitive to IV: IV contraction in the back month can hurt long calendars.

- Directional risk: Large moves away from the strike reduce value.

- Assignment logistics: Short front-month options can be assigned; plan rolls and exits accordingly.

- Complexity: Requires monitoring of time, volatility, and event risk.

For broader context on aligning tactics with your horizon, review our guide to long term vs. short term investment strategies.

Next Steps for Mastering Calendar Spreads

Calendars convert a view on time and volatility into a defined-risk position. Start with liquid underlyings, align strikes with your outlook, and size positions to account for IV shifts and assignment management. Track realized outcomes across different tickers and regimes to refine entry and roll criteria.

If you want checklists for selecting expirations and strikes, examples based on current SPY term structures, and templates for rolling decisions, consider Above the Green Line memberships for tools and step-by-step education.

Related Articles

[pt_view id=”9b64b383ox”]